The debate between IRA and 401(k) plans is crucial for anyone looking to secure their financial future. Choosing the right retirement savings option can significantly impact your financial stability in your golden years. Both Individual Retirement Accounts (IRA) and 401(k) plans have unique features that cater to different financial situations and goals. Understanding these differences can help you make an informed decision that aligns with your retirement objectives.

In this comprehensive guide, we will delve into the intricacies of IRA and 401(k) plans, examining their benefits, drawbacks, and suitability based on individual circumstances. We will also provide you with insights on how to maximize your retirement savings effectively. By the end of this article, you will have a clear understanding of which option may be best for you.

As retirement approaches, the importance of strategic financial planning cannot be overstated. Whether you're a young professional beginning your savings journey or someone closer to retirement seeking to optimize your existing savings, understanding IRA vs 401(k) is essential. Let’s dive deep into the details.

Table of Contents

- What is an IRA?

- What is a 401(k)?

- Key Differences Between IRA and 401(k)

- Contribution Limits of IRA and 401(k)

- Tax Implications of IRA and 401(k)

- Withdrawal Rules for IRA and 401(k)

- Pros and Cons of IRA and 401(k)

- Choosing the Right Option for You

- Conclusion

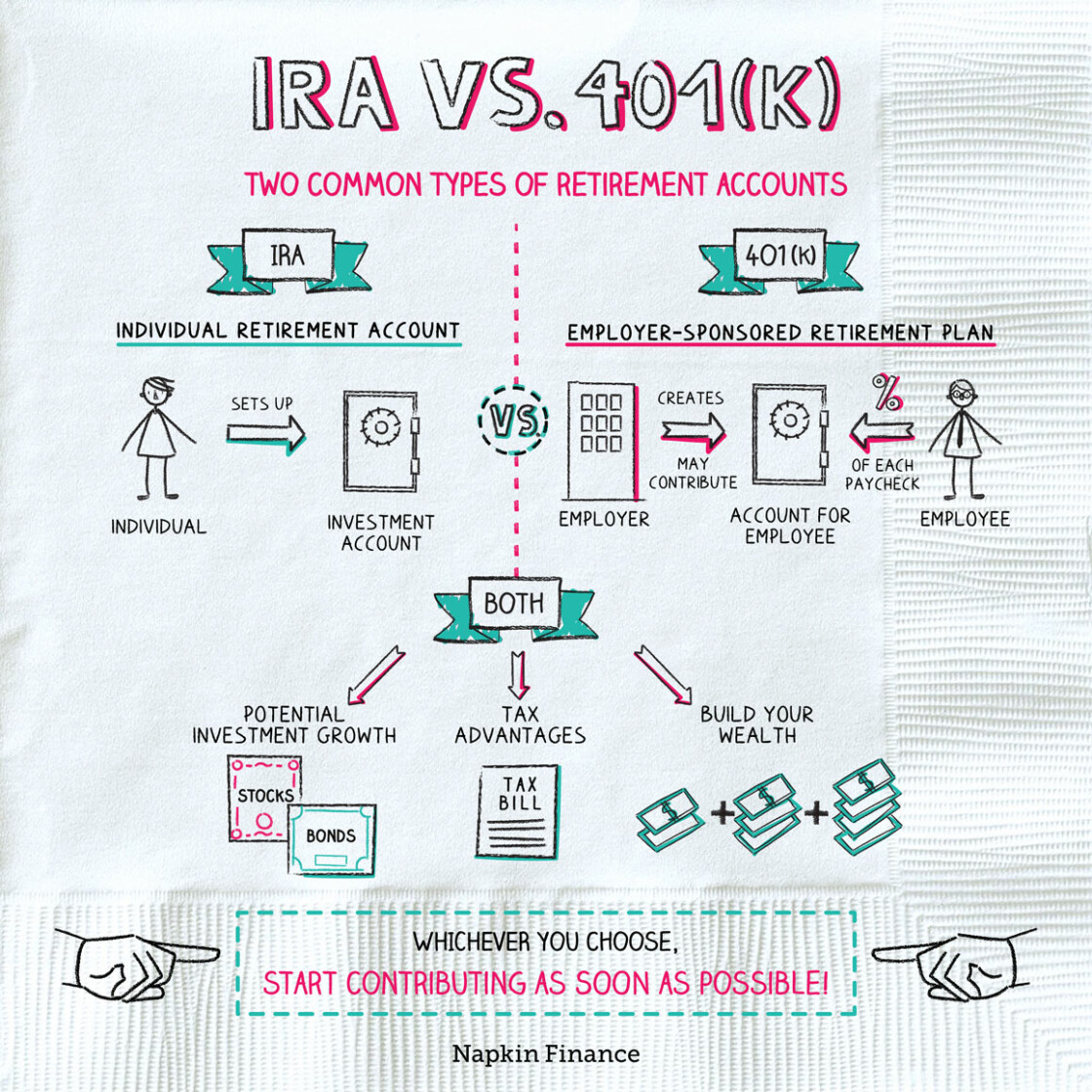

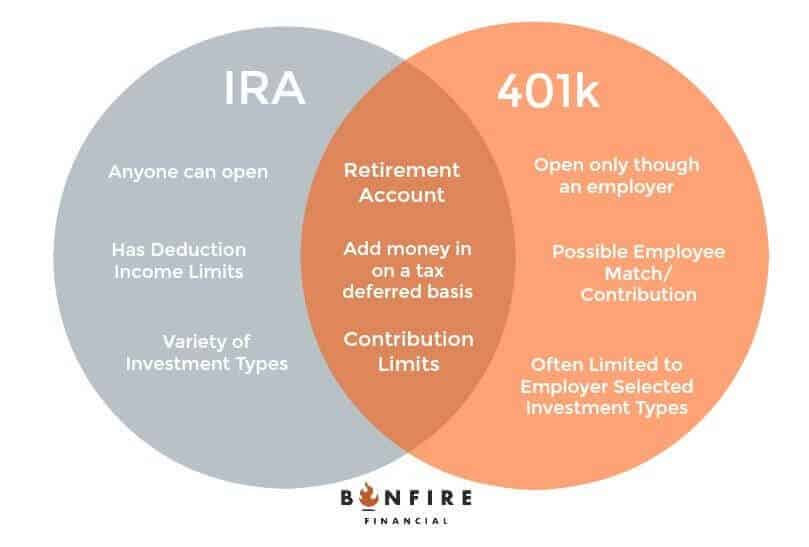

What is an IRA?

An Individual Retirement Account (IRA) is a personal savings plan that provides tax advantages for retirement savings. Individuals can open an IRA through banks, investment firms, or other financial institutions. There are several types of IRAs, including Traditional IRAs, Roth IRAs, and SEP IRAs, each with distinct features and tax implications.

Types of IRAs

- Traditional IRA: Contributions may be tax-deductible, and taxes are paid upon withdrawal.

- Roth IRA: Contributions are made with after-tax income, allowing for tax-free withdrawals in retirement.

- SEP IRA: Designed for self-employed individuals or small business owners, allowing higher contribution limits.

What is a 401(k)?

A 401(k) is an employer-sponsored retirement savings plan that allows employees to save a portion of their paycheck before taxes are taken out. Employers may offer matching contributions, making it a powerful tool for building retirement savings. There are two primary types of 401(k) plans: Traditional 401(k) and Roth 401(k).

Types of 401(k)s

- Traditional 401(k): Contributions are made pre-tax, and taxes are paid upon withdrawal.

- Roth 401(k): Contributions are made after-tax, enabling tax-free withdrawals in retirement.

Key Differences Between IRA and 401(k)

While both IRA and 401(k) plans serve the same purpose of retirement savings, they have several key differences that may influence your decision:

- Contribution Limits: 401(k) plans typically have higher annual contribution limits compared to IRAs.

- Employer Contributions: Employers can match contributions in a 401(k), whereas IRAs do not have this feature.

- Investment Choices: IRAs often provide a broader range of investment options compared to 401(k) plans, which may be limited to the employer's selected funds.

- Tax Treatment: Both plans offer tax advantages, but the timing of tax payments differs based on the type of account.

Contribution Limits of IRA and 401(k)

The contribution limits for both IRAs and 401(k)s are set by the IRS and can change annually. For 2023, the limits are as follows:

- Traditional and Roth IRA: $6,500 for individuals under 50; $7,500 for those 50 and older.

- 401(k): $22,500 for individuals under 50; $30,000 for those 50 and older, including catch-up contributions.

These limits are crucial for maximizing your retirement savings and ensuring you take full advantage of tax benefits.

Tax Implications of IRA and 401(k)

Understanding the tax implications of IRA and 401(k) accounts is essential for effective retirement planning:

- Traditional IRA: Contributions may be tax-deductible, reducing your taxable income in the year you contribute. However, withdrawals in retirement are taxed as ordinary income.

- Roth IRA: Contributions are made with after-tax dollars, allowing for tax-free growth and withdrawals in retirement.

- Traditional 401(k): Contributions are pre-tax, lowering your taxable income, but withdrawals are taxed in retirement.

- Roth 401(k): Contributions are made after-tax, similar to a Roth IRA, allowing for tax-free withdrawals.

Withdrawal Rules for IRA and 401(k)

Both IRAs and 401(k)s have specific rules regarding withdrawals that can affect your retirement planning:

- Traditional IRA: Withdrawals before age 59½ may incur a 10% penalty, in addition to regular income tax.

- Roth IRA: Contributions can be withdrawn tax-free at any time; however, earnings are subject to penalties if withdrawn before age 59½ unless certain conditions are met.

- 401(k): Withdrawals before age 59½ are generally subject to a 10% penalty, along with regular income tax.

Pros and Cons of IRA and 401(k)

When deciding between IRA and 401(k), it is important to consider the advantages and disadvantages of each:

Pros of IRA

- Wider range of investment options.

- Potential tax-free withdrawals with a Roth IRA.

- Ability to open an account independently.

Cons of IRA

- Lower contribution limits compared to 401(k).

- No employer matching contributions.

Pros of 401(k)

- Higher contribution limits.

- Employer matching contributions boost savings.

- Automatic payroll deductions make saving easier.

Cons of 401(k)

- Limited investment options.

- Potentially high fees depending on the plan.

Choosing the Right Option for You

Deciding between an IRA and a 401(k) depends on your individual financial situation, goals, and employment status:

- If your employer offers a 401(k) with matching contributions, consider contributing enough to receive the full match.

- If you are self-employed or want more control over your investments, an IRA may be a better choice.

- Consider your current tax situation and future expectations when choosing between traditional and Roth options.

Conclusion

In conclusion, both IRA and 401(k) plans offer valuable opportunities for retirement savings, each with distinct features and benefits. Understanding the differences between IRA vs 401(k) is essential for making informed decisions about your financial future. Consider your personal circumstances, goals, and tax implications when choosing the best retirement savings option for you.

We encourage you to share your thoughts in the comments below, explore more articles on retirement planning, and take charge of your financial future today!

Thank you for reading, and we hope you found this guide on IRA vs 401(k) informative and helpful. We invite you to return for more insights on financial planning and retirement strategies.

You Might Also Like

Understanding Bleeding During Ovulation: Causes, Symptoms, And When To Seek HelpExploring The Mystique Of The Red String Of Fate

C Sharp: A Comprehensive Guide To Understanding And Mastering C# Programming

Call Of Duty Makarov: The Infamous Anti-Hero Of Modern Warfare

Exploring The Phenomenon Of 1D: A Comprehensive Guide To One Direction

Article Recommendations

- Ruben Roman

- Travis Kelce August 2024

- Future Opportunities_0.xml

- Clr Soak Overnight

- Business Tactics_0.xml

- Ella Bleu S Career Updates

- Arianna Lima 2024

- Lax Plane Spotting Locations

- Daryl Hannah

- Ne Yo