FDIC insurance limits are crucial for anyone looking to safeguard their deposits in banks and credit unions. In today’s financial landscape, understanding these limits can make a significant difference in how you manage your savings and investments. This article will delve into the intricacies of FDIC insurance, its limits, and how you can protect your hard-earned money.

As an account holder, it’s essential to know what FDIC insurance covers and the maximum amount you can insure. This knowledge not only gives you peace of mind but also ensures that you can make informed decisions about where and how to save your money. In this comprehensive guide, we will explore various aspects of FDIC insurance limits, including eligibility, types of accounts covered, and strategies for maximizing your insurance coverage.

Whether you are an individual saver or a business owner, understanding FDIC insurance is vital for managing your finances effectively. Join us as we break down the important details of FDIC insurance limits and learn how to ensure your deposits are well protected.

Table of Contents

- What Is FDIC Insurance?

- FDIC Insurance Limits Explained

- Types of Accounts Covered by FDIC Insurance

- How Does FDIC Insurance Work?

- Maximizing Your FDIC Insurance Coverage

- Common Misconceptions About FDIC Insurance

- FDIC Insurance and Cryptocurrency

- Conclusion

What Is FDIC Insurance?

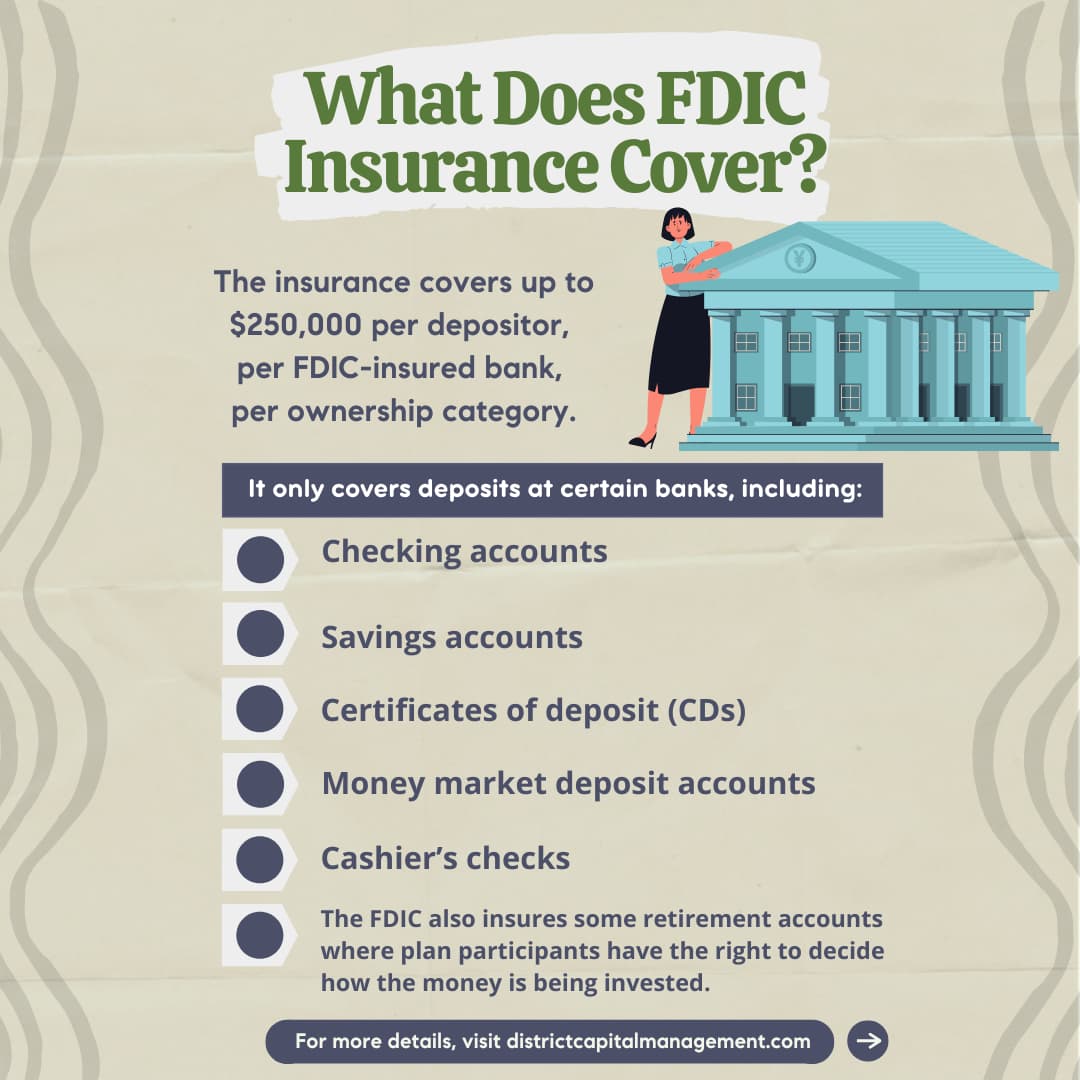

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that was created in 1933. Its primary purpose is to maintain public confidence in the nation’s financial system by protecting depositors. FDIC insurance provides coverage for deposits made at insured banks and savings institutions. If a bank fails, the FDIC ensures that depositors receive their money back, up to the insurance limit.

FDIC Insurance Limits Explained

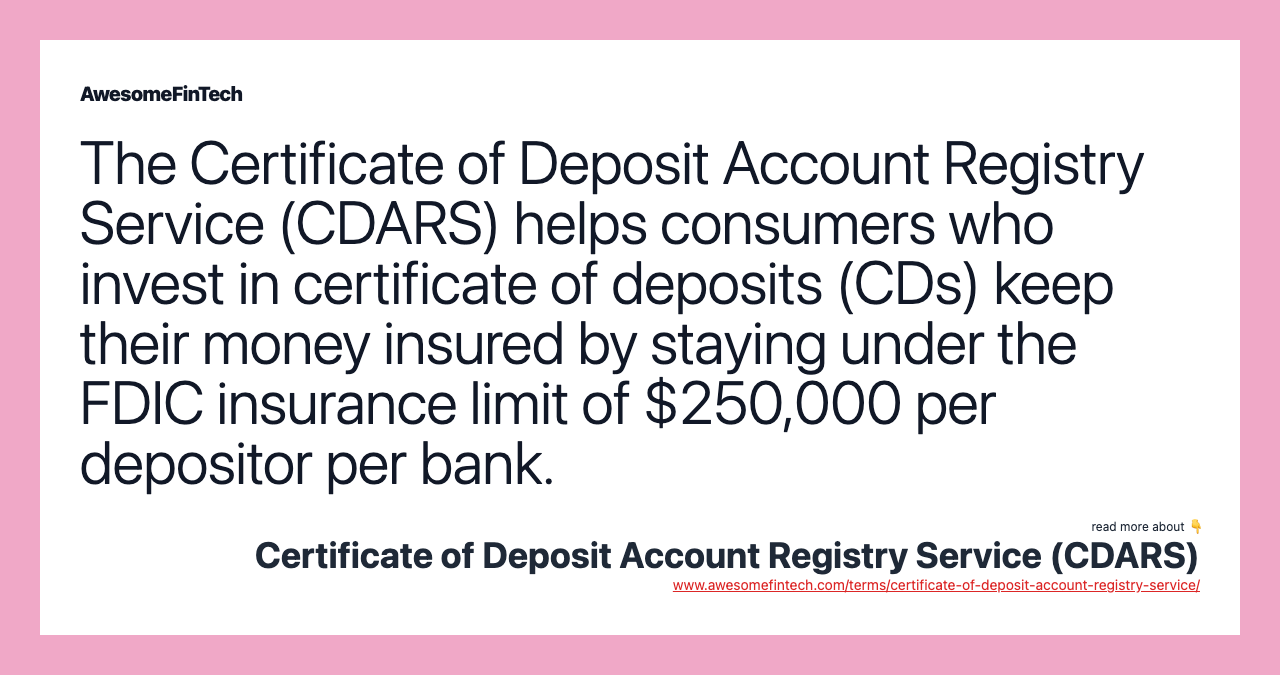

As of 2023, the standard FDIC insurance limit is $250,000 per depositor, per insured bank, for each account ownership category. This means that if you have multiple types of accounts—such as individual accounts, joint accounts, and retirement accounts—the coverage could potentially be higher.

- **Individual Accounts:** Each depositor is insured up to $250,000.

- **Joint Accounts:** Each co-owner of a joint account is insured up to $250,000.

- **Retirement Accounts:** Accounts like IRAs are covered up to $250,000.

- **Trust Accounts:** The coverage can vary depending on the beneficiaries.

Types of Accounts Covered by FDIC Insurance

FDIC insurance covers various types of deposit accounts, which include:

- Savings Accounts: Traditional savings accounts are fully insured.

- Checking Accounts: Funds in checking accounts are also protected.

- Money Market Accounts: These accounts, which might offer higher interest rates, are covered as well.

- Certificates of Deposit (CDs): CDs are insured up to the same limit.

How Does FDIC Insurance Work?

FDIC insurance works by protecting depositors in the event of a bank failure. When a bank goes bankrupt, the FDIC steps in to pay depositors their insured amounts. This process typically occurs within a few days. If your deposits exceed the insurance limit, you may lose the excess amount unless you take steps to ensure coverage.

Maximizing Your FDIC Insurance Coverage

To maximize your FDIC insurance coverage, consider the following strategies:

- Open Accounts at Different Banks: By spreading your deposits across multiple banks, you can ensure that more of your money is insured.

- Utilize Different Ownership Categories: Open accounts in various ownership categories to increase coverage.

- Monitor Your Deposits: Keep track of your total deposits to avoid exceeding the insurance limit.

Common Misconceptions About FDIC Insurance

Many people have misconceptions about FDIC insurance. Some common myths include:

- **FDIC Insurance Covers All Financial Products:** Not all financial products are covered; for instance, stocks, bonds, and mutual funds are not insured.

- **Joint Accounts Are Insured for One Amount:** Each co-owner of a joint account is insured up to the limit, providing additional coverage.

FDIC Insurance and Cryptocurrency

As cryptocurrency gains popularity, many wonder about its insurance status. FDIC insurance does not cover cryptocurrencies directly. However, if you hold USD in a bank that is FDIC insured, that specific amount is protected. Always check with your bank regarding their policies on cryptocurrency transactions.

Conclusion

Understanding FDIC insurance limits is crucial for anyone looking to safeguard their funds. With the standard insurance limit set at $250,000 per depositor, per bank, it’s essential to be strategic about how you manage your deposits. By spreading your money across different banks and account types, you can maximize your coverage and ensure that your finances are secure.

We invite you to share your thoughts on FDIC insurance in the comments below, and feel free to explore our other articles for more financial insights.

Thank you for reading! We hope this article has provided valuable information to help you make informed decisions about your finances. Be sure to visit us again for more tips and guides on financial literacy.

You Might Also Like

Finding The Best Ukulele Lessons Near Me: A Comprehensive GuideAffresh: The Ultimate Solution For Cleaning Your Appliances

Exploring Stamford: A Comprehensive Guide To The City

All You Need To Know About Chartreux Cats: The Feline Marvel

Discovering DuckDuckGo: The Ultimate Privacy-Focused Search Engine

Article Recommendations

- Ella Bleu S Career Updates

- Water Softener Overflowing Brine Tank

- Deacon Johnson

- Kylie Jenner Before Surgery

- Piper Parabo

- Lola Consuelos Weight Loss Ozempic

- Long Handled Post Hole Diggers

- Hig Roberts

- Girl Meets World Cast

- Creative Solutions_0.xml

:max_bytes(150000):strip_icc()/FDIC_Seal_by_Matthew_Bisanz-b92facd3f0304834b33c305f7f9b2007.jpeg)