Choosing the right life insurance policy can be a daunting task, especially when deciding between term and permanent life insurance. With the increasing complexity of financial products, it's essential to understand the differences and benefits of each type to make an informed decision. In this article, we will explore the features, advantages, and potential drawbacks of both term and permanent life insurance, helping you determine which option aligns best with your financial goals.

Life insurance serves as a crucial safety net for your loved ones, providing financial security in the event of your untimely demise. However, the choice between term and permanent life insurance is significant, as it can impact your long-term financial planning. By understanding the nuances of these two types of insurance, you can ensure that you select the right policy that meets your needs and those of your family.

This comprehensive guide will delve into various aspects of term vs permanent life insurance, including their definitions, benefits, costs, and ideal scenarios for each type. By the end of this article, you will be equipped with the knowledge necessary to make a well-informed decision about your life insurance options.

Table of Contents

- What is Term Life Insurance?

- Benefits of Term Life Insurance

- Drawbacks of Term Life Insurance

- What is Permanent Life Insurance?

- Benefits of Permanent Life Insurance

- Drawbacks of Permanent Life Insurance

- Term vs Permanent Life Insurance: Key Differences

- Which is Right for You?

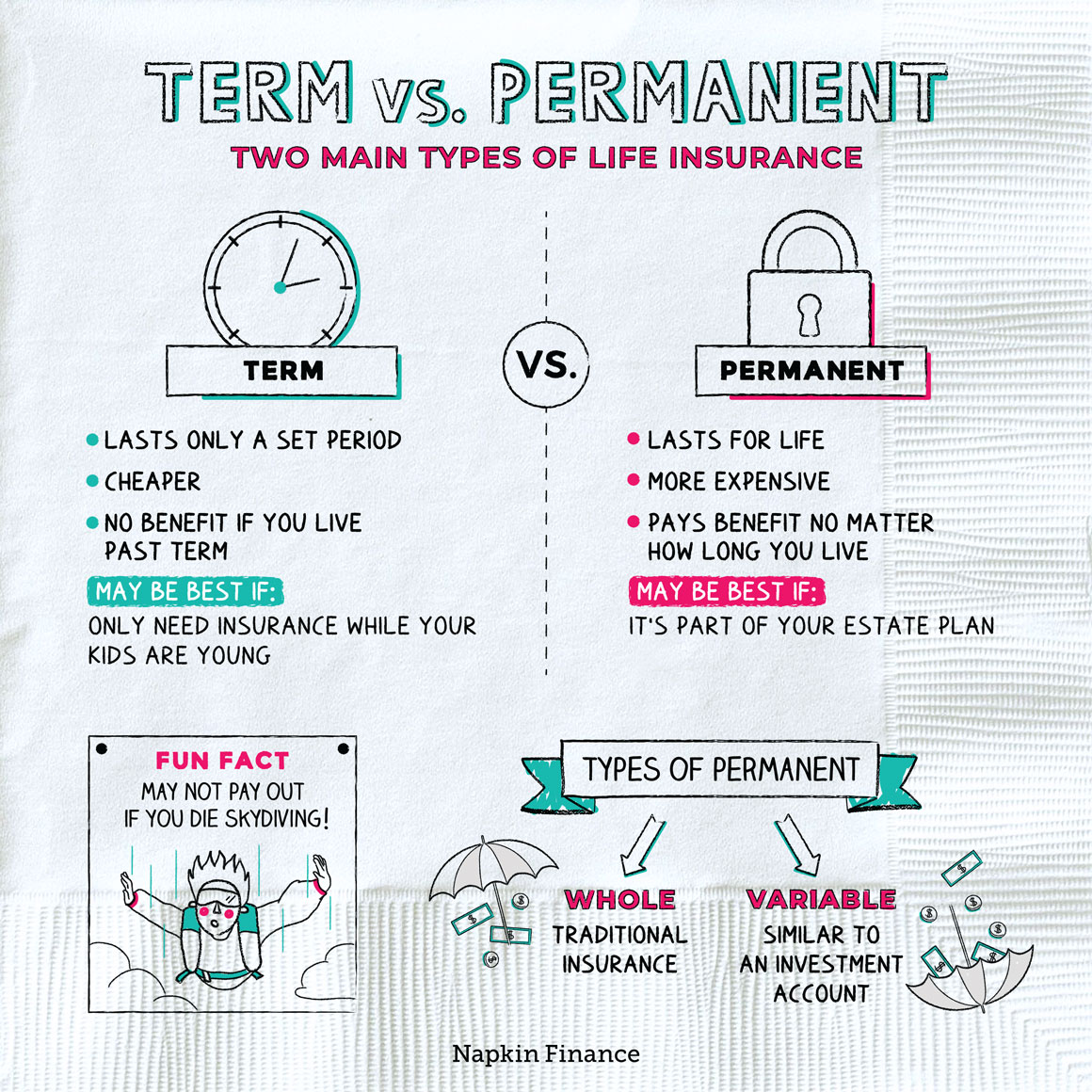

What is Term Life Insurance?

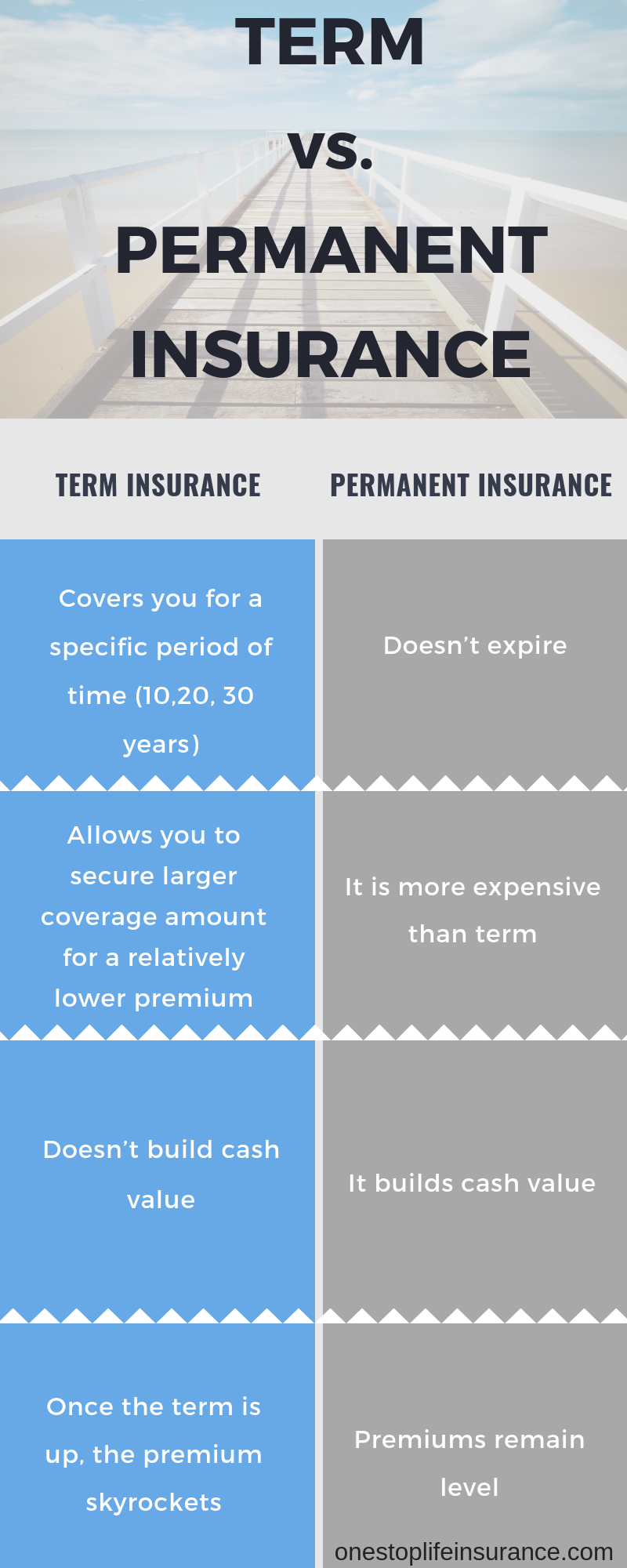

Term life insurance is a type of life insurance policy that provides coverage for a specified period, typically ranging from 10 to 30 years. During this term, if the insured person passes away, the beneficiaries receive a death benefit. If the policyholder survives the term, the coverage ends, and there is no payout.

Characteristics of Term Life Insurance

- Coverage is temporary, lasting only for the duration of the term.

- Generally more affordable than permanent life insurance.

- Does not accumulate cash value.

- Renewable or convertible options may be available.

Benefits of Term Life Insurance

Term life insurance offers several advantages that make it an attractive option for many individuals:

- Affordability: Term policies typically have lower premiums than permanent policies, making them accessible for families on a budget.

- Flexibility: Policyholders can choose the term length that aligns with their financial obligations, such as raising children or paying off a mortgage.

- Simple Structure: Term life insurance is straightforward, with fewer complexities than permanent policies.

Drawbacks of Term Life Insurance

Despite its advantages, term life insurance also has some disadvantages to consider:

- No Cash Value: Unlike permanent policies, term life insurance does not build cash value over time.

- Coverage Ends: If the term expires and the insured does not renew, there is no payout, leaving beneficiaries without financial support.

- Premium Increases: Renewing a term policy may result in higher premiums as the insured ages.

What is Permanent Life Insurance?

Permanently life insurance provides lifelong coverage, as long as premiums are paid. This type of insurance includes several subtypes, such as whole life, universal life, and variable life insurance. Permanent life insurance policies accumulate cash value over time, which can be borrowed against or withdrawn.

Types of Permanent Life Insurance

- Whole Life Insurance: Provides a fixed premium and guaranteed cash value accumulation.

- Universal Life Insurance: Offers flexible premiums and adjustable death benefits.

- Variable Life Insurance: Allows policyholders to invest cash value in various investment options, potentially increasing returns.

Benefits of Permanent Life Insurance

Permanent life insurance comes with multiple benefits, including:

- Lifelong Coverage: Provides coverage for the entire life of the insured, ensuring financial support for beneficiaries no matter when death occurs.

- Cash Value Accumulation: Builds cash value that grows tax-deferred, providing a savings component.

- Flexible Premiums: Some policies allow for premium adjustments based on the policyholder's financial situation.

Drawbacks of Permanent Life Insurance

However, permanent life insurance may not be suitable for everyone. Some drawbacks include:

- Higher Premiums: Permanent policies typically have higher premiums than term policies, which can strain budgets.

- Complexity: The various components and options can be overwhelming for policyholders.

- Potential for Loss: If the cash value investments perform poorly, the policyholder could lose money.

Term vs Permanent Life Insurance: Key Differences

When comparing term and permanent life insurance, several key differences emerge:

| Feature | Term Life Insurance | Permanent Life Insurance |

|---|---|---|

| Duration of Coverage | Temporary (10-30 years) | Lifelong |

| Premium Costs | Generally lower | Generally higher |

| Cash Value | No | Yes |

| Flexibility | Limited | More flexible |

| Renewal | May increase premiums | N/A |

Which is Right for You?

Determining whether term or permanent life insurance is right for you depends on various factors, including your financial situation, family needs, and long-term goals:

- Choose Term Life Insurance if:

- You are looking for affordable coverage for a specific period, such as while raising children or paying off debts.

- You prefer a straightforward insurance product without cash value components.

- You want to ensure your beneficiaries are financially secure during your working years.

- Choose Permanent Life Insurance if:

- You want lifelong coverage and are willing to pay higher premiums for that security.

- You seek a policy that builds cash value over time for future financial needs.

- You want the flexibility to adjust premiums and coverage as your financial situation changes.

Conclusion

In summary, understanding the differences between term and permanent life insurance is crucial for making informed financial decisions. Each type of policy has its unique benefits and drawbacks, and the right choice depends on your individual circumstances and goals. We encourage you to assess your financial needs, consider your budget, and consult with a licensed insurance agent to determine the best life insurance solution for you and your family.

If you found this article helpful, please leave a comment below, share it with others, and explore more insightful articles on our site to enhance your financial knowledge.

Final Thoughts

Life insurance is an essential component of financial planning, ensuring that your loved ones are protected in the event of your passing. Whether you choose term or permanent life insurance, the key is to understand your needs and make informed decisions that provide the best financial security for your family. We look forward to seeing you back on our site for more valuable insights!

You Might Also Like

Understanding Tooth Decay Symptoms: A Comprehensive GuideHow To Get Oil Out Of Concrete: Effective Methods For Stain Removal

How Long To Fry Chicken Wings: The Ultimate Guide To Perfectly Crispy Wings

Best Auto Insurance In Texas: A Comprehensive Guide

Understanding The Meaning Of JW: What Does JW Mean?

Article Recommendations

- Dinosaur Dung

- Lava Stone Bracelet Essential Oil

- Cost To Extend Garage

- Collision Repair Before And After

- Risk Territory Between Ukraine And Siberia Nyt

- Travis Kelce August 2024

- Jennifer Syme Crash

- Lola Consuelos Weight Loss Ozempic

- How Old Is Adriana Lima 2024

- Growth Hacking_0.xml