When it comes to choosing the right life insurance policy, understanding the differences between term life insurance and whole life insurance is crucial. Each type of policy offers distinct advantages and disadvantages that cater to different financial needs and goals. In this comprehensive guide, we will explore the ins and outs of term life insurance versus whole life insurance, helping you make an informed decision on which policy might be best suited for you and your loved ones.

Life insurance is not just a financial product; it's a safety net that ensures your family’s financial stability in the event of your untimely demise. By delving into the characteristics, benefits, and drawbacks of both term and whole life insurance, we aim to equip you with the knowledge necessary to make a wise investment in your family's future. Whether you’re a first-time buyer or reevaluating your current policy, this article will provide valuable insights.

In this article, we will also discuss the financial implications of each type of policy, the potential for cash value accumulation, and additional riders that can enhance your coverage. Let’s dive into the details, starting with a clear definition of both term and whole life insurance policies.

Table of Contents

- Definition of Term Life and Whole Life Insurance

- Key Differences Between Term Life and Whole Life Insurance

- Pros and Cons of Term Life Insurance

- Pros and Cons of Whole Life Insurance

- Financial Implications of Each Policy

- Cash Value Accumulation in Whole Life Insurance

- Policy Riders and Options

- Conclusion

Definition of Term Life and Whole Life Insurance

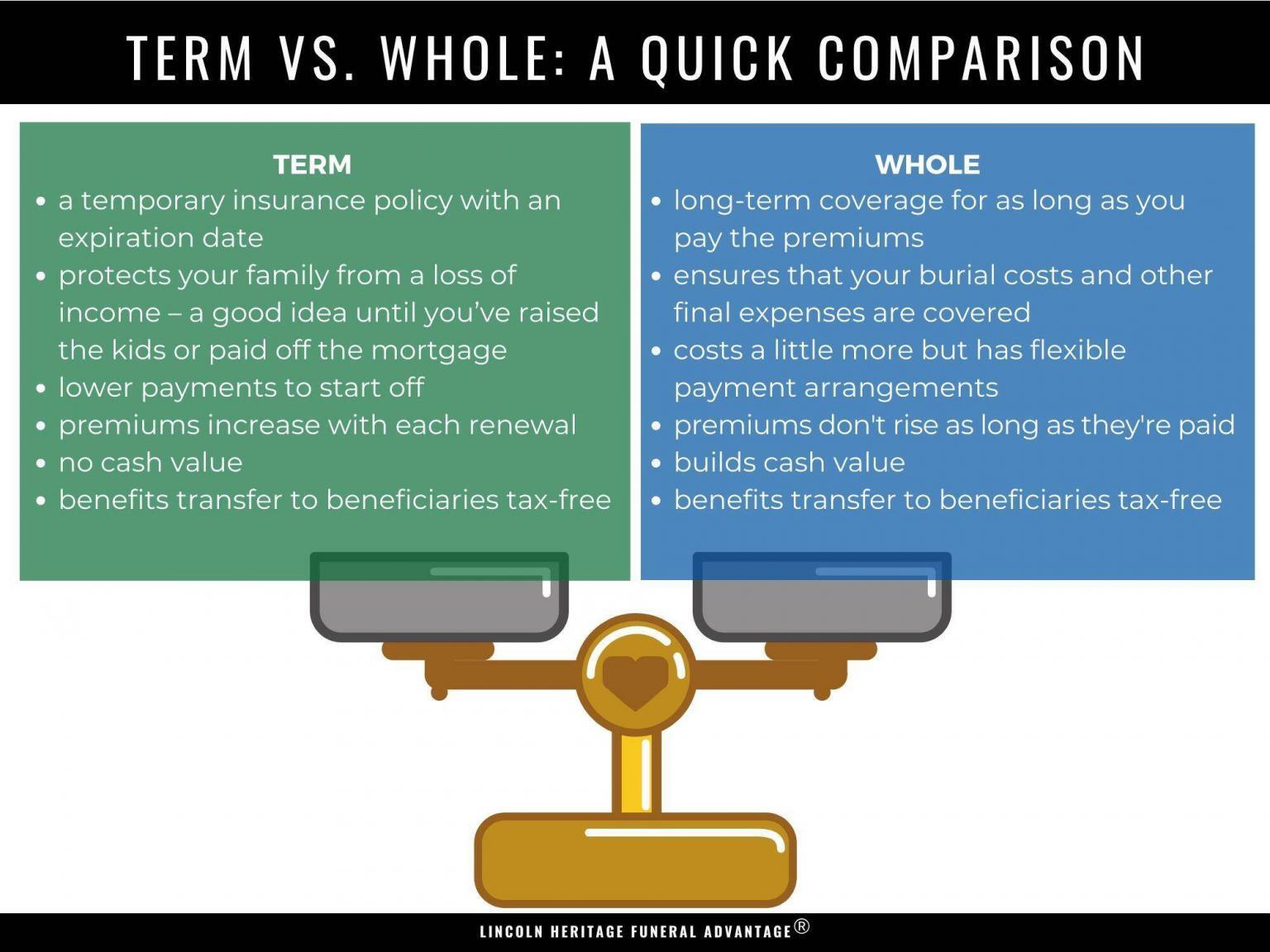

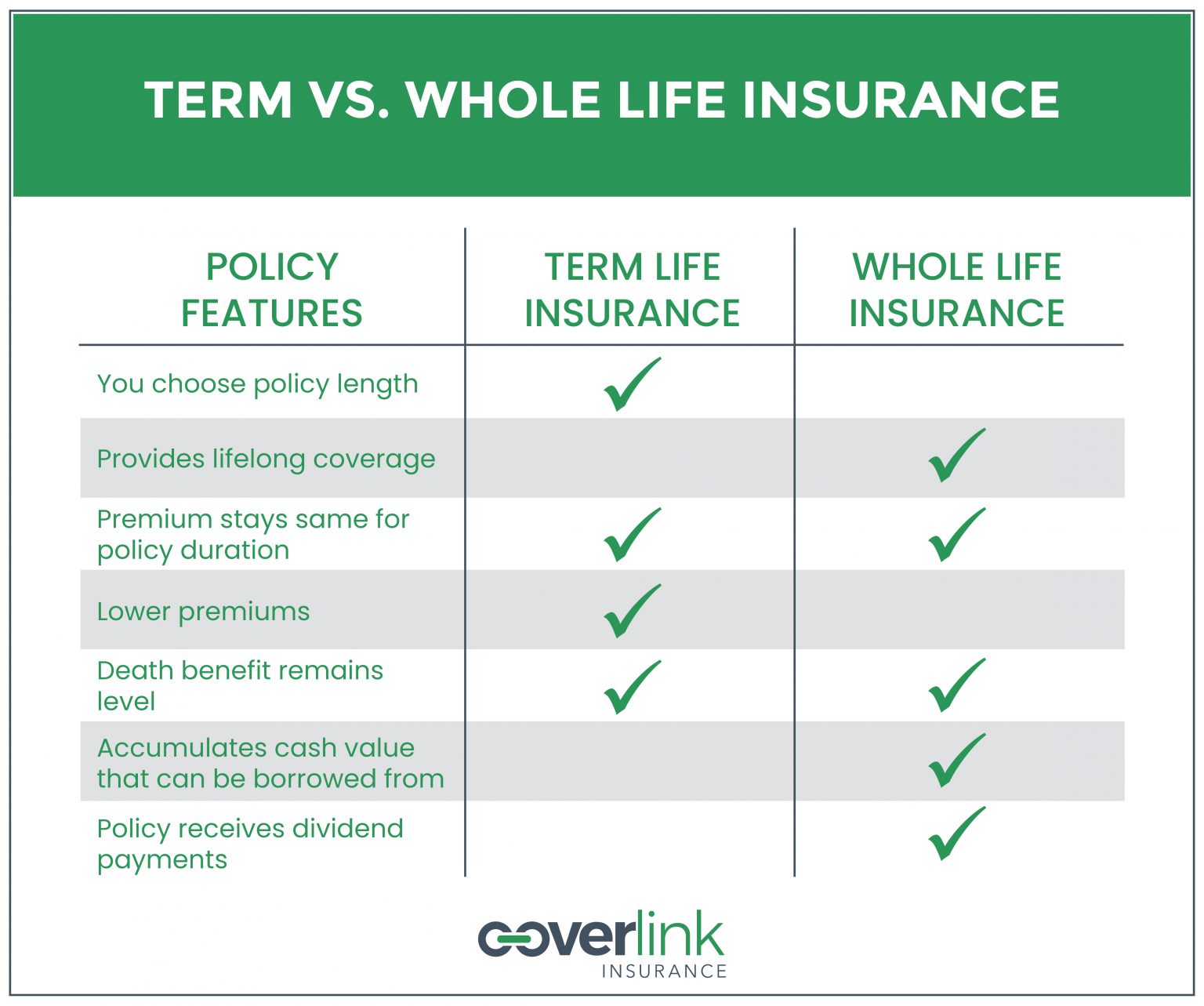

Term life insurance provides coverage for a specific period, typically ranging from 10 to 30 years. If the insured passes away during the term, the beneficiaries receive a death benefit. If the term expires and the policyholder is still alive, there is no payout, and the policy will need to be renewed or converted to a permanent policy.

On the other hand, whole life insurance is a type of permanent life insurance that provides coverage for the insured’s entire lifetime, as long as premiums are paid. In addition to a death benefit, whole life policies accumulate cash value over time, which can be borrowed against or withdrawn in certain circumstances.

Key Differences Between Term Life and Whole Life Insurance

Understanding the key differences between term life and whole life insurance can help you assess which option aligns better with your financial goals. Here are the primary distinctions:

- Duration of Coverage: Term life offers coverage for a set period, while whole life provides lifetime coverage.

- Premiums: Term life typically has lower premiums compared to whole life, which are generally higher due to the cash value component.

- Cash Value: Whole life policies accumulate cash value, whereas term life does not.

- Investment Component: Whole life functions as both insurance and an investment, while term life is purely protective.

Pros and Cons of Term Life Insurance

Advantages of Term Life Insurance

- Affordability: Term life insurance is usually more budget-friendly, making it accessible for young families.

- Flexibility: Policyholders can choose coverage lengths that fit their needs, which can be particularly useful for temporary financial obligations.

- Easy to Understand: The straightforward nature of term policies makes them easy to comprehend.

Disadvantages of Term Life Insurance

- Temporary Coverage: Once the term ends, coverage ceases unless renewed, which may lead to higher premiums or denial of coverage due to health changes.

- No Cash Value: Term policies do not build cash value, which means no return on premiums paid if the policyholder outlives the term.

Pros and Cons of Whole Life Insurance

Advantages of Whole Life Insurance

- Lifetime Coverage: Whole life insurance guarantees coverage for the insured’s lifetime.

- Cash Value Accumulation: Policies build cash value over time, which can be borrowed against or withdrawn.

- Fixed Premiums: Premiums generally remain constant throughout the life of the policy.

Disadvantages of Whole Life Insurance

- Higher Premiums: Whole life insurance typically comes with higher premiums compared to term life, which may not be affordable for everyone.

- Complexity: The structure of whole life policies can be more complicated, requiring a deeper understanding of cash value and dividends.

Financial Implications of Each Policy

When considering the financial implications of term life and whole life insurance, it's essential to evaluate your long-term financial goals. Term life insurance is often recommended for those looking for affordable coverage to protect their family during high-expense years, such as raising children or paying off a mortgage.

Conversely, whole life insurance can serve as a long-term financial strategy. The cash value component provides a safety net that can be utilized for emergencies, retirement funding, or other financial needs. However, the higher premiums must be factored into your overall budget.

Cash Value Accumulation in Whole Life Insurance

One of the most significant advantages of whole life insurance is its cash value accumulation. As you pay premiums, a portion goes towards building cash value, which grows at a guaranteed rate. This cash value can be accessed through loans or withdrawals, providing financial flexibility.

However, it’s essential to note that borrowing against your cash value will reduce the death benefit, and unpaid loans accrue interest, potentially impacting your policy’s overall value.

Policy Riders and Options

Both term and whole life insurance policies can come with various riders and options that enhance coverage. Common riders include:

- Accidental Death Benefit: Provides an additional death benefit if the insured dies from an accident.

- Waiver of Premium: Waives premiums if the policyholder becomes disabled.

- Child Rider: Adds coverage for the insured's children.

These riders can offer added protection and flexibility, allowing policyholders to tailor their insurance to their specific needs.

Conclusion

Deciding between term life insurance and whole life insurance ultimately depends on your individual financial situation and goals. Term life is ideal for those seeking affordable coverage for a specific period, while whole life insurance offers the benefits of lifelong coverage and cash value accumulation.

Before making a decision, it’s wise to consult with a financial advisor or insurance professional to assess your unique circumstances. Don’t hesitate to leave your comments below, share this article with friends or family seeking guidance in their insurance choices, and explore our other informative articles on financial planning.

Final Thoughts

We hope this article has provided valuable insights into the differences between term life insurance and whole life insurance. Understanding these options empowers you to make informed decisions that will benefit you and your loved ones for years to come. Thank you for reading, and we look forward to welcoming you back to our site for more insightful content.

You Might Also Like

Mineta MHA: The Unique Character In My Hero AcademiaUnveiling The Mysteries Of The Hittites: An Ancient Civilization

Homemade Ant Killer: Effective Solutions For A Pest-Free Home

Best Index Funds To Invest In: A Comprehensive Guide

Understanding Code Phone 44: What You Need To Know

Article Recommendations

- Travis Kelce August 2024

- Legal Seafood Recipes Crab Cakes

- Michael Jordan Tequila Reposado

- Mia Hamm Soccer Player

- Corinne Foxx

- Water Softener Overflowing Brine Tank

- Efficient Strategies_0.xml

- Business Tactics_0.xml

- Active Smooth Nail Polish

- Collision Repair Before And After

:max_bytes(150000):strip_icc()/dotdash-term-life-vs-whole-life-5075430-Final-60fb4e8f7bae43e0a65a3fac2431479c.jpg)