Homeowners insurance is a crucial aspect of protecting your investment in your home. It provides financial coverage in the event of damage or loss due to various risks, such as fire, theft, or natural disasters. However, many homeowners are left wondering about the average cost of homeowners insurance and how it compares to their budget. In this comprehensive guide, we will explore everything you need to know about homeowners insurance costs, factors that influence premiums, and tips for finding the best coverage.

In the United States, the average cost of homeowners insurance can vary significantly based on several factors, including location, property value, and the level of coverage desired. Understanding these variables is essential for homeowners looking to protect their assets without breaking the bank. Moreover, with the rise of climate-related events and increasing home values, knowing how to navigate homeowners insurance costs has become more crucial than ever.

This article will provide a detailed breakdown of the average cost of homeowners insurance, insights into how rates are calculated, and practical tips for saving on your premiums. Whether you are a first-time homeowner or looking to reassess your current policy, this guide will equip you with the knowledge you need to make informed decisions about your homeowners insurance.

Table of Contents

- Average Cost of Homeowners Insurance

- Factors Influencing Homeowners Insurance Costs

- How Are Homeowners Insurance Rates Calculated?

- Regional Variations in Homeowners Insurance Costs

- Types of Homeowners Insurance Coverage

- Tips for Saving on Homeowners Insurance

- Common Misconceptions About Homeowners Insurance

- Conclusion

Average Cost of Homeowners Insurance

The average cost of homeowners insurance in the United States is approximately $1,500 per year, but this figure can vary widely. According to the National Association of Insurance Commissioners (NAIC), homeowners insurance premiums have been steadily increasing over the past decade, reflecting changes in the housing market and the increasing frequency of natural disasters.

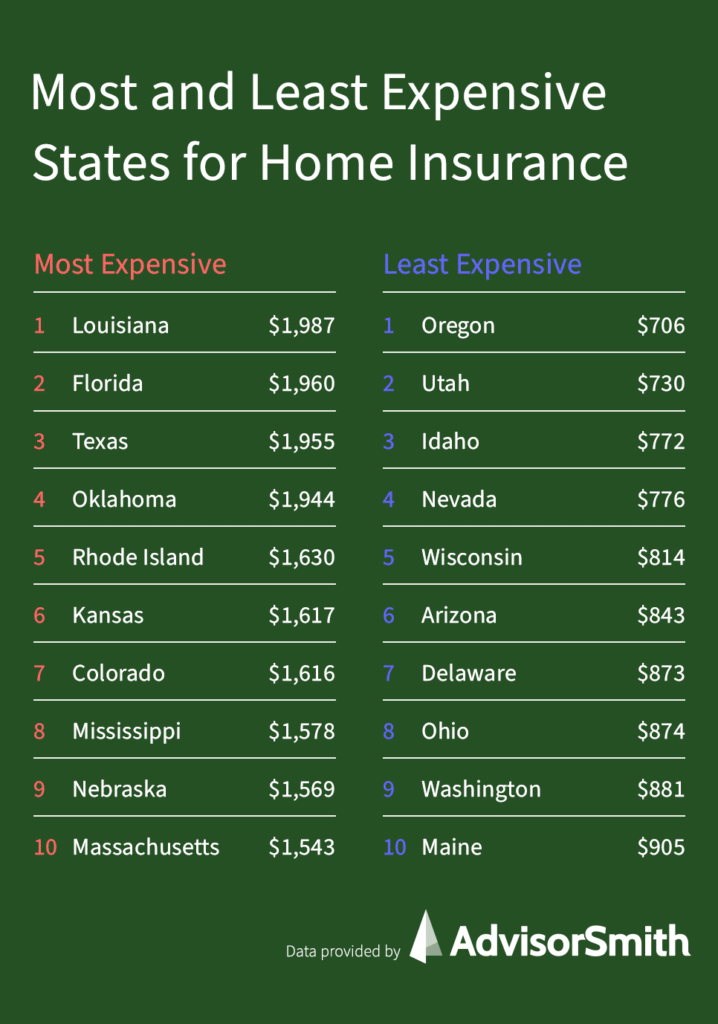

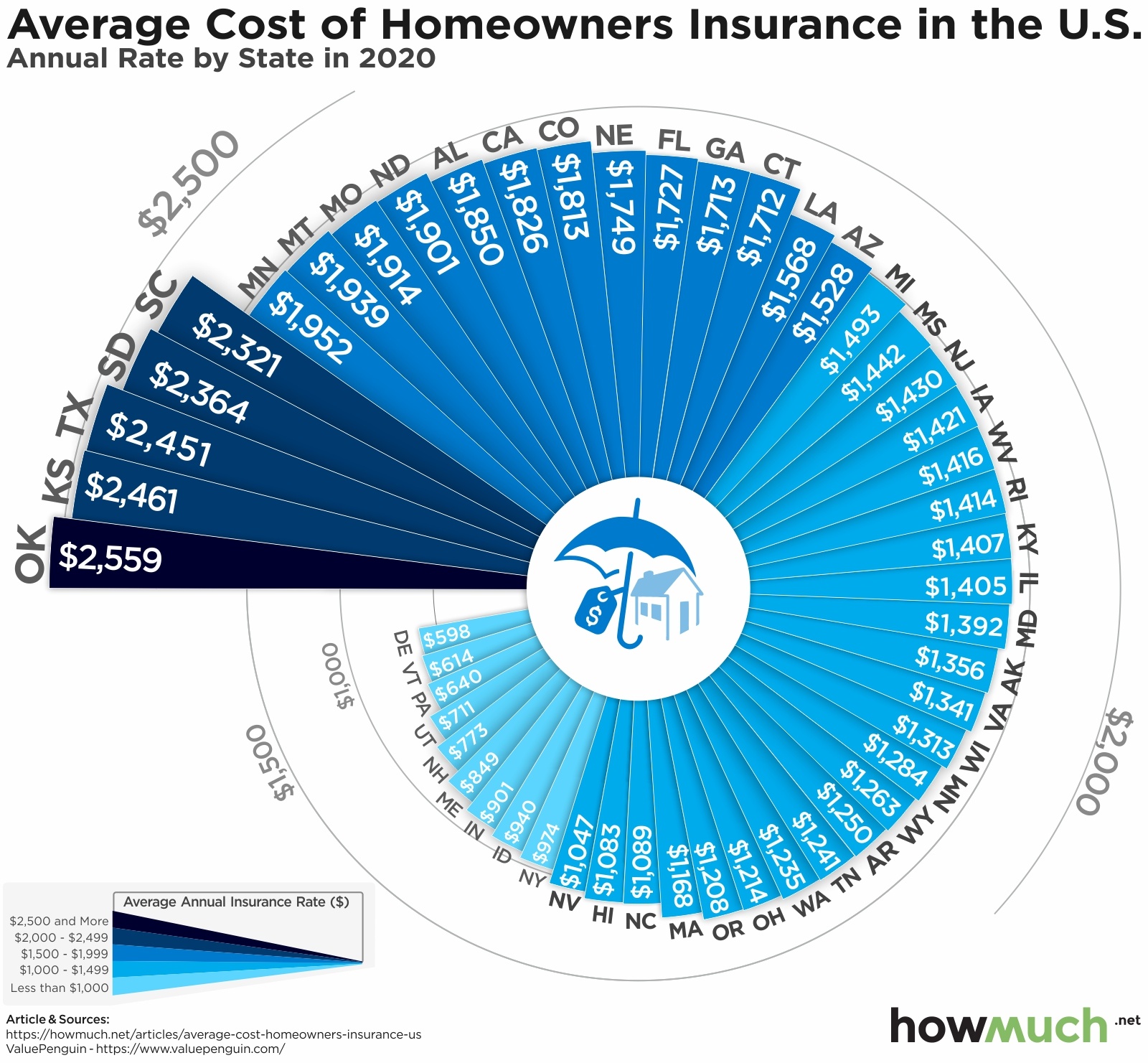

National Averages by State

- California: $1,000 - $2,000

- Texas: $1,200 - $2,500

- Florida: $1,500 - $3,500

- New York: $800 - $1,800

These averages highlight the importance of shopping around for the best rates and understanding that geographic location plays a significant role in determining homeowners insurance costs.

Factors Influencing Homeowners Insurance Costs

Several factors influence the cost of homeowners insurance premiums. Understanding these factors can help homeowners identify potential savings and make informed choices about their coverage.

1. Location

Your home's location is one of the most significant factors affecting your insurance premiums. Areas prone to natural disasters, such as hurricanes, floods, or wildfires, typically have higher insurance costs.

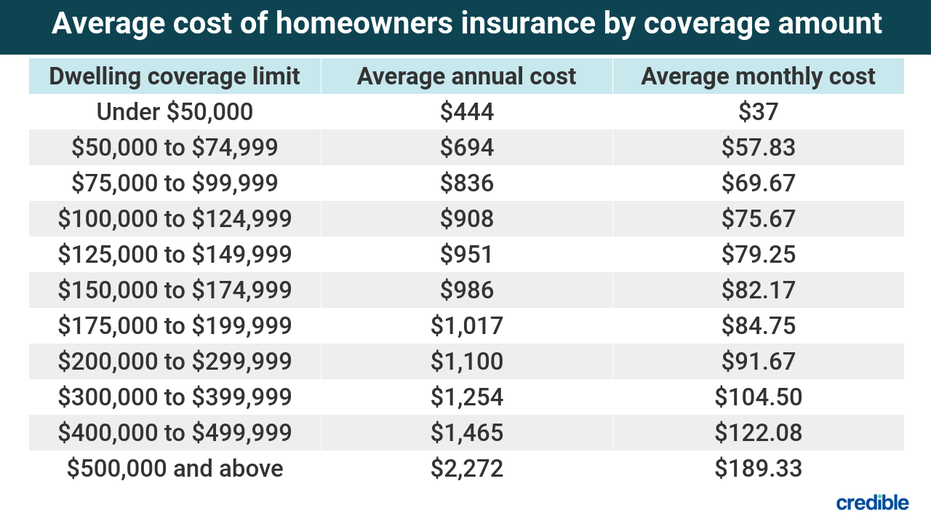

2. Home Value and Replacement Cost

The value of your home and the cost to replace it directly impact your insurance premium. More expensive homes generally require higher coverage limits, resulting in increased premiums.

3. Claims History

If you have a history of filing insurance claims, insurers may view you as a higher risk, leading to increased premiums. Maintaining a claims-free record can help keep your rates lower.

4. Coverage Limits and Deductibles

The level of coverage you choose and the deductible amount you are willing to pay can significantly impact your premium. Higher coverage limits and lower deductibles result in higher premiums, while the opposite can help lower costs.

How Are Homeowners Insurance Rates Calculated?

Homeowners insurance rates are calculated using a complex algorithm that takes into account various risk factors and statistical data. Insurance companies utilize underwriting guidelines to assess risk and determine appropriate premiums.

Some of the key elements considered in rate calculations include:

- Your credit score

- The age and condition of your home

- Local crime rates

- Recent natural disasters in your area

Regional Variations in Homeowners Insurance Costs

Homeowners insurance costs can vary significantly from one region to another. For example, states with higher risks of natural disasters, such as Florida and Texas, often face higher premiums compared to states with lower risks like Vermont or Wisconsin. Understanding these regional variations can help homeowners make informed decisions about their coverage.

Coastal vs. Inland Areas

Coastal areas are typically more vulnerable to hurricanes and flooding, leading to higher insurance premiums. In contrast, inland areas may have lower premiums due to reduced risk.

Urban vs. Rural Areas

Urban areas often have higher crime rates, which can impact insurance costs. Conversely, rural areas may face lower premiums due to lower crime rates and less risk of certain disasters.

Types of Homeowners Insurance Coverage

Understanding the different types of homeowners insurance coverage is essential for selecting the right policy for your needs. Here are the most common types of coverage:

1. Dwelling Coverage

This coverage protects the structure of your home against damages from covered perils, such as fire or theft.

2. Personal Property Coverage

This type of coverage protects your personal belongings, including furniture, electronics, and clothing, from covered risks.

3. Liability Coverage

Liability coverage protects you from claims made against you by others for bodily injury or property damage that occurs on your property.

4. Additional Living Expenses (ALE)

ALE coverage helps cover costs for temporary housing and living expenses if your home becomes uninhabitable due to a covered loss.

Tips for Saving on Homeowners Insurance

Finding ways to save on homeowners insurance is essential for homeowners looking to manage their budgets effectively. Here are some practical tips:

- Shop around and compare quotes from multiple insurers.

- Increase your deductible to lower your premium.

- Bundle your homeowners insurance with other policies, such as auto insurance.

- Take advantage of discounts for security systems and smoke detectors.

- Maintain a good credit score to qualify for lower rates.

Common Misconceptions About Homeowners Insurance

There are several misconceptions surrounding homeowners insurance that can lead to confusion. Here are a few common myths debunked:

- Myth: Homeowners insurance covers all types of damage.

- Myth: Flood damage is always covered under standard policies.

- Myth: Homeowners insurance is optional.

Understanding the truth behind these myths can help homeowners make informed decisions about their insurance needs.

Conclusion

In conclusion, the average cost of homeowners insurance is influenced by several factors, including location, home value, and coverage options. By understanding how rates are calculated and exploring different types of coverage, homeowners can make informed choices that protect their investments while saving money.

If you're looking to secure the best homeowners insurance policy for your needs, take the time to shop around, compare quotes, and consult with insurance professionals. Feel free to leave a comment below or share this article with friends and family who may benefit from this information.

We hope this guide has provided valuable insights into the average cost of homeowners insurance. Remember to stay informed and revisit our site for more helpful articles in the future!

You Might Also Like

Understanding Gluten Intolerance: Symptoms, Causes, And ManagementWhat Is A 1040 Tax Form? Understanding The Essential Tax Document

Knees Hurt After Running: Understanding The Causes And Solutions

What Kills Epstein-Barr Virus: Understanding And Managing EBV

Creative Indoor Activities For Kids: Fun And Engaging Options

Article Recommendations

- Brand Building_0.xml

- Digital Revolution_0.xml

- Sheryl Lowe Age

- Cost To Extend Garage

- Water Softener Overflowing Brine Tank

- Business Tactics_0.xml

- How To Make Raphael In Infinite Craft

- Dinosaur Dung

- Claudine Blanchard Crimes

- Kamila Valieva