Leasing a car offers numerous advantages, including the ability to drive a new model with the latest features, without the long-term commitment of ownership. It can be an excellent option for those who enjoy changing cars frequently and want to avoid the hassles of selling a used car. This guide will explore the key aspects of car leasing, helping you navigate the maze of options and find the best deal near you. The process of leasing can seem daunting with various terms and conditions, but it doesn't have to be. With the right information and guidance, you can confidently lease a car that suits your lifestyle and budget. This comprehensive article will walk you through the process, answer common questions, and provide tips on negotiating the best lease terms. So, buckle up and let's get started on your journey to leasing the perfect car near you!

Table of Contents

- Understanding Leasing: What It Entails

- Benefits of Leasing Cars Near Me

- Leasing vs. Buying: Making the Right Choice

- How to Lease a Car: Step-by-Step Guide

- Negotiating a Lease: Tips and Tricks

- Understanding Lease Terms and Conditions

- Calculating Lease Payments: What to Expect

- Finding the Best Lease Deals Near Me

- End of Lease Options: What Happens Next?

- Leasing Tips for First-Time Lessees

- Common Mistakes to Avoid When Leasing

- Leasing Economy Cars vs. Luxury Cars

- Leasing Cars for Business: A Smart Move?

- Environmental Impact of Leasing vs. Buying

- Frequently Asked Questions

- Conclusion

Understanding Leasing: What It Entails

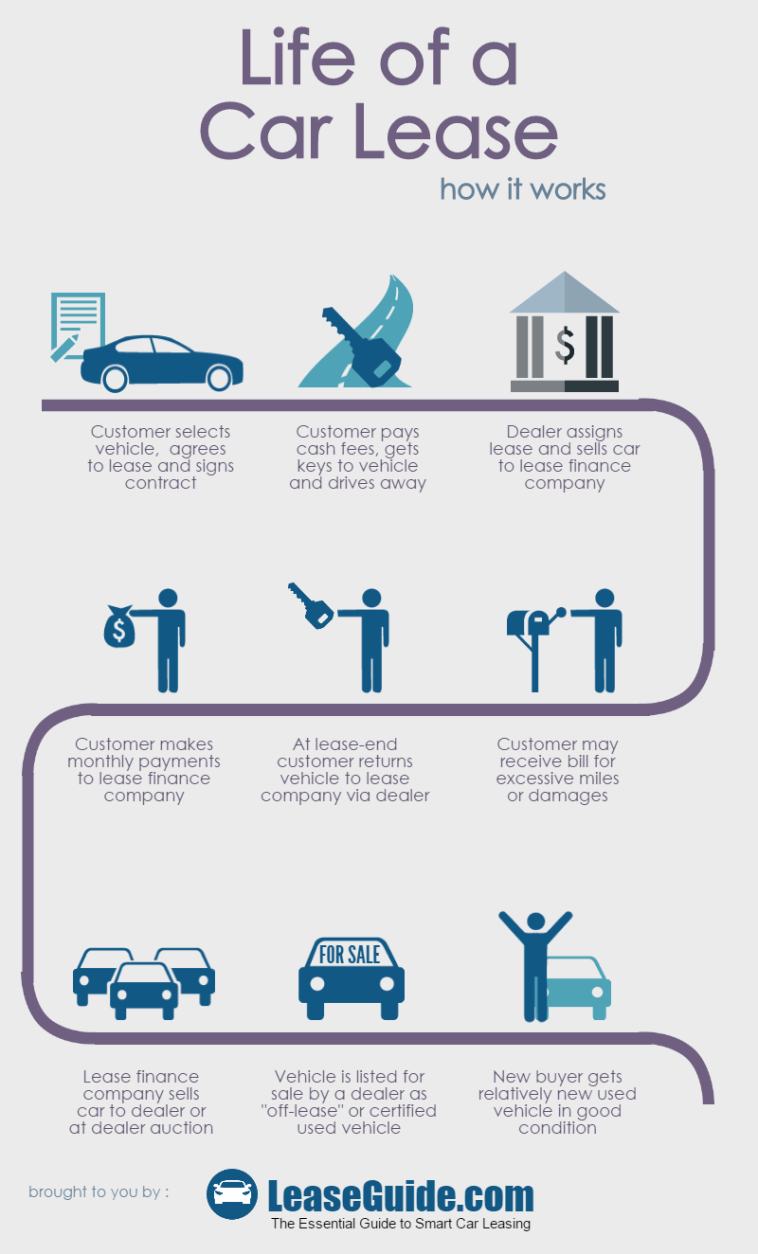

Leasing a car involves essentially renting it for a specified period, typically between two to four years. Unlike purchasing, where you own the vehicle outright after paying off the loan, leasing allows you to use the car for the lease term and then return it to the dealership. This arrangement means you are only paying for the car's depreciation during the lease period, plus interest and fees, rather than the full price.

When leasing, you'll sign a lease agreement that outlines the terms, including the lease period, monthly payment, mileage limits, and any wear-and-tear policies. It's crucial to read and understand these terms before signing, as they dictate your responsibilities and costs throughout the lease.

One of the appealing aspects of leasing is the lower monthly payments compared to buying. This is because you're not financing the entire value of the car, just the portion you use. Additionally, leases often require lower down payments, making it easier for many to afford a newer or more luxurious vehicle than they could if purchasing outright.

However, it's important to consider the limitations of leasing. These can include mileage restrictions, typically ranging from 10,000 to 15,000 miles per year, which can incur additional fees if exceeded. There's also the responsibility of maintaining the car in good condition, as excessive wear and tear can lead to extra charges at the end of the lease.

Overall, leasing can be an excellent choice for those who value driving the latest models and prefer lower monthly payments. It's especially beneficial for individuals who don't drive long distances and are comfortable with adhering to the lease terms.

Benefits of Leasing Cars Near Me

Leasing cars near you offers a multitude of benefits that can make it an attractive option for many drivers. One of the most significant advantages is the chance to drive a new car every few years, complete with the latest technology, safety features, and improved fuel efficiency. This means you can enjoy the perks of a new vehicle without the commitment of long-term ownership.

Another major benefit is the cost savings associated with leasing. Typically, lease payments are lower than loan payments when buying a car. This is because you are only paying for the car's depreciation over the lease term, plus interest and fees. Additionally, leases often require a smaller down payment, making it easier to access higher-end vehicles that might be out of reach if purchasing.

Leasing also provides a level of convenience and flexibility. At the end of the lease, you can simply return the car to the dealership and choose a new model to lease, without the hassle of selling a used car. This can be particularly appealing for those who like to change vehicles frequently and enjoy driving the latest models.

Moreover, leasing can offer tax advantages, especially for business owners. Lease payments may be deductible as a business expense, reducing your taxable income. It's essential to consult with a tax professional to understand how leasing can impact your specific situation.

Lastly, leasing can provide peace of mind. Most leases come with warranty coverage that lasts the duration of the lease term, covering many potential repair costs. This means fewer unexpected expenses and more predictable budgeting for maintenance.

Overall, the benefits of leasing cars near you can make it a wise choice for those seeking affordability, flexibility, and access to the latest automotive technology.

Leasing vs. Buying: Making the Right Choice

When deciding between leasing and buying a car, it's important to consider your lifestyle, financial situation, and personal preferences. Both options have their pros and cons, and understanding these can help you make an informed decision.

Leasing, as discussed, offers lower monthly payments, the ability to drive a new car every few years, and reduced maintenance headaches thanks to warranty coverage. It's ideal for those who don't drive long distances and want to avoid the depreciation and resale concerns associated with car ownership.

On the other hand, buying a car provides the benefit of ownership. Once you've paid off the loan, the vehicle is yours, and you're free from monthly payments. Ownership allows you to build equity in the car and potentially sell it for a profit in the future. Additionally, there are no mileage restrictions or wear-and-tear penalties, giving you more freedom in how you use the vehicle.

However, buying a car often requires a larger down payment and higher monthly payments than leasing. It also means bearing the full brunt of the vehicle's depreciation, which can be significant in the first few years. For those who prefer to keep their vehicles long-term, buying can be more economical in the long run.

Ultimately, the choice between leasing and buying depends on your priorities. If you value driving new cars, lower upfront costs, and predictable expenses, leasing may be the better option. However, if you prefer to own your vehicle, enjoy customization, and plan to keep it for many years, buying might be the way to go.

How to Lease a Car: Step-by-Step Guide

Leasing a car involves several steps, from choosing the right vehicle to signing the lease agreement. Here's a step-by-step guide to help you navigate the process:

- Determine Your Budget: Start by assessing your budget to determine how much you can afford to spend on a lease payment each month. Consider additional costs such as insurance, maintenance, and potential excess mileage fees.

- Choose the Right Vehicle: Research different makes and models to find a car that fits your needs and budget. Consider factors such as fuel efficiency, safety features, and the total cost of ownership.

- Find a Dealership: Look for dealerships near you that offer leasing options on your preferred vehicle. It's a good idea to compare offers from multiple dealerships to find the best deal.

- Negotiate the Lease Terms: Once you've selected a dealership, negotiate the lease terms, including the monthly payment, mileage limit, and any additional fees. Be sure to read and understand the lease agreement before signing.

- Finalize the Lease Agreement: After negotiating the terms, you'll need to complete the necessary paperwork and provide any required documentation, such as proof of insurance and identification.

- Take Delivery of the Vehicle: Once the paperwork is complete, you can take delivery of your leased vehicle. Be sure to inspect the car thoroughly and familiarize yourself with its features before driving off the lot.

By following these steps, you can successfully lease a car that meets your needs and budget, ensuring a smooth and satisfying leasing experience.

Negotiating a Lease: Tips and Tricks

Negotiating a lease can be daunting, but with the right approach and preparation, you can secure favorable terms. Here are some tips and tricks to help you negotiate effectively:

- Research the Market: Before heading to the dealership, research the current market conditions, including average lease prices for your desired vehicle. This information can give you leverage during negotiations.

- Know Your Credit Score: Your credit score plays a crucial role in determining your lease terms. A higher score can qualify you for better rates, so be sure to check your credit report and address any issues before negotiating.

- Focus on the Total Lease Cost: Instead of solely concentrating on the monthly payment, consider the total cost of the lease, including interest, fees, and potential mileage penalties. This approach will give you a clearer picture of the overall expense.

- Be Prepared to Walk Away: If the dealership isn't willing to meet your terms, be prepared to walk away. Sometimes, showing that you're willing to leave can encourage the dealer to offer better terms.

- Consider Multiple Dealerships: Don't limit yourself to one dealership. Get quotes from multiple dealers and use them as leverage to negotiate a better deal.

With these strategies, you can confidently negotiate a lease that aligns with your budget and driving needs.

Understanding Lease Terms and Conditions

Before signing a lease agreement, it's essential to understand the terms and conditions, as they outline your responsibilities and obligations throughout the lease. Here are some key elements to consider:

- Lease Term: This refers to the duration of the lease, typically ranging from 24 to 48 months. Consider your driving habits and preferences when choosing the lease term.

- Mileage Limit: Leases often include mileage limits, typically between 10,000 and 15,000 miles per year. Exceeding this limit can result in additional fees, so choose a limit that aligns with your driving habits.

- Residual Value: The residual value is the car's estimated worth at the end of the lease term. It affects your monthly payments and can impact your decision to purchase the vehicle at the end of the lease.

- Money Factor: The money factor, similar to the interest rate on a loan, determines the cost of financing the lease. A lower money factor means lower monthly payments, so negotiate for the best rate possible.

- Wear-and-Tear Policy: Understand the lease's wear-and-tear policy, as excessive wear can lead to additional charges. Keep the vehicle in good condition to avoid these fees.

By thoroughly reviewing and understanding these terms, you can enter a lease agreement with confidence, knowing what to expect throughout the lease period.

Calculating Lease Payments: What to Expect

Calculating lease payments involves considering several factors, including the car's price, residual value, money factor, and lease term. Here's a breakdown of how these elements contribute to your monthly payment:

- Capitalized Cost: This is the agreed-upon price of the vehicle, including any additional fees or taxes. The lower the capitalized cost, the lower your monthly payments.

- Residual Value: The car's estimated value at the end of the lease term. A higher residual value means lower monthly payments, as you're financing a smaller portion of the car's depreciation.

- Money Factor: The interest rate of the lease, expressed as a decimal. A lower money factor results in lower monthly payments, so negotiate for the best rate possible.

- Lease Term: The duration of the lease affects your monthly payments. Shorter lease terms typically result in higher payments, while longer terms can lower them.

By understanding these factors, you can better estimate your monthly lease payments and choose a vehicle that fits your budget.

Finding the Best Lease Deals Near Me

To find the best lease deals near you, start by researching local dealerships and comparing offers from multiple sources. Here are some tips to help you find the best deals:

- Check Online Resources: Use websites and apps that aggregate lease deals from various dealerships. These resources can help you compare offers and find the best deals in your area.

- Visit Dealership Websites: Many dealerships list special lease offers on their websites, so it's worth checking their promotions before visiting in person.

- Timing Matters: Dealerships often offer better deals at the end of the month or quarter when they're trying to meet sales targets. Consider timing your lease negotiations to take advantage of these incentives.

- Consider Manufacturer Offers: Automakers occasionally offer special lease incentives, such as reduced interest rates or cashback offers. Keep an eye on manufacturer promotions to find the best deal.

By following these tips, you can find the best lease deals near you and secure a vehicle that meets your needs and budget.

End of Lease Options: What Happens Next?

As your lease term comes to an end, you'll need to decide what to do with your leased vehicle. Here are your options:

- Return the Vehicle: The most common option is returning the vehicle to the dealership. Ensure the car is in good condition and within the mileage limits to avoid additional fees.

- Purchase the Vehicle: If you love the car and want to keep it, consider purchasing it at the end of the lease. The lease agreement will specify the purchase price, often based on the residual value.

- Lease a New Vehicle: Many lessees choose to lease a new vehicle, allowing them to drive a different model with the latest features. This option provides continuity and flexibility.

Understanding your end-of-lease options allows you to make an informed decision that aligns with your needs and preferences.

Leasing Tips for First-Time Lessees

If you're leasing a car for the first time, here are some tips to help you navigate the process:

- Research Thoroughly: Take the time to research different makes, models, and lease offers. Being well-informed will help you make better decisions and secure favorable terms.

- Understand the Terms: Familiarize yourself with key lease terms, including mileage limits, residual value, and wear-and-tear policies. This knowledge will help you avoid unexpected fees.

- Know Your Budget: Determine a realistic budget for your lease payments and stick to it. Factor in additional costs like insurance and maintenance when setting your budget.

- Inspect the Vehicle: Before taking delivery, thoroughly inspect the vehicle for any damage or issues. Report any concerns to the dealership to avoid being held accountable later.

- Keep the Car Maintained: Regular maintenance is crucial to avoid wear-and-tear fees at the end of the lease. Follow the manufacturer's recommended service schedule and keep records of all maintenance work.

By following these tips, you'll be well-prepared for your first leasing experience, ensuring a smooth and satisfying process.

Common Mistakes to Avoid When Leasing

Leasing a car can be a great option, but it's essential to avoid common mistakes that can lead to unexpected expenses and frustration. Here are some pitfalls to watch out for:

- Underestimating Mileage: One of the most common mistakes is underestimating how much you'll drive. Exceeding the mileage limit can result in costly overage fees, so choose a limit that matches your driving habits.

- Ignoring Wear-and-Tear Policies: Failing to maintain the vehicle or ignoring wear-and-tear policies can lead to additional charges at the end of the lease. Keep the car in good condition to avoid these fees.

- Not Negotiating Terms: Many lessees accept the first lease offer without negotiating. Remember, lease terms are often negotiable, so don't hesitate to ask for better rates or incentives.

- Overlooking Additional Costs: Be aware of additional costs, such as acquisition fees, disposition fees, and excess mileage charges. These can add up and impact your overall lease cost.

By avoiding these common mistakes, you can make the most of your leasing experience and enjoy the benefits of driving a new car.

Leasing Economy Cars vs. Luxury Cars

When it comes to leasing cars, you have a wide range of options, from economical compact cars to luxurious high-end vehicles. Understanding the differences between leasing economy cars and luxury cars can help you make the right choice for your needs and budget.

Leasing economy cars, such as compact sedans or hatchbacks, tends to be more affordable due to their lower purchase price and depreciation. These vehicles often offer excellent fuel efficiency and lower maintenance costs, making them a practical choice for budget-conscious individuals or those with a long daily commute. Additionally, economy cars typically have lower insurance premiums, further reducing the overall cost of leasing.

On the other hand, leasing luxury cars offers the opportunity to drive a high-end vehicle with advanced features and superior craftsmanship. Luxury cars often come equipped with cutting-edge technology, premium materials, and enhanced performance capabilities, providing a more enjoyable and comfortable driving experience. While the monthly payments for leasing luxury cars may be higher, the prestige and satisfaction they offer can be worth the cost for some lessees.

When deciding between leasing economy or luxury cars, consider your budget, lifestyle, and personal preferences. If you prioritize cost-effectiveness and practicality, an economy car may be the better choice. However, if you value luxury, performance, and advanced features, a luxury car lease might be worth the investment.

Leasing Cars for Business: A Smart Move?

Leasing cars for business purposes can offer several advantages, making it a smart move for many companies. Whether you're a small business owner or managing a fleet for a larger corporation, leasing can provide flexibility, cost savings, and tax benefits.

One of the main benefits of leasing cars for business is the ability to conserve capital. Leasing typically requires a lower upfront investment compared to purchasing, allowing businesses to allocate resources to other critical areas. Additionally, the predictable monthly payments make budgeting easier and help manage cash flow more effectively.

Leasing also offers flexibility, enabling businesses to adapt their vehicle fleet to changing needs. As your business grows or changes, you can easily upgrade or switch to different vehicles at the end of the lease term, ensuring your fleet remains up-to-date and efficient. This flexibility is particularly valuable for businesses that require specific vehicles for different projects or clients.

Furthermore, leasing can provide tax advantages. Lease payments are often considered a business expense and may be deductible, reducing your taxable income. This deduction can lead to significant tax savings, making leasing an attractive option for many businesses.

However, it's essential to carefully review the lease terms and conditions, including mileage limits and wear-and-tear policies, to ensure they align with your business needs. By considering these factors, you can determine whether leasing cars for business is the right choice for your company.

Environmental Impact of Leasing vs. Buying

When considering the environmental impact of leasing versus buying a car, it's important to evaluate the entire lifecycle of the vehicle, from production to disposal. Both leasing and buying have their ecological pros and cons, and understanding these can help you make a more sustainable choice.

Leasing can have a lower environmental impact in some cases, as it encourages the use of newer vehicles with improved fuel efficiency and lower emissions. By regularly updating to the latest models, lessees can benefit from advances in green technology, such as hybrid or electric vehicles, which can significantly reduce their carbon footprint. Additionally, leasing can help ensure that older, less efficient vehicles are taken off the road and replaced with cleaner alternatives.

However, the frequent turnover of leased vehicles can also contribute to increased production demands, leading to higher resource consumption and emissions during the manufacturing process. As a result, leasing may not always be the most environmentally friendly option, especially if the lessee frequently upgrades to new vehicles.

Buying a car, on the other hand, allows you to keep and maintain the vehicle for a longer period, reducing the need for new production and the associated environmental impact. However, older vehicles can become less fuel-efficient and produce more emissions over time, offsetting some of the environmental benefits of long-term ownership.

Ultimately, the environmental impact of leasing versus buying will depend on various factors, including the type of vehicle, driving habits, and maintenance practices. Opting for fuel-efficient or electric vehicles, regardless of whether you lease or buy, can help minimize your ecological footprint and contribute to a more sustainable future.

Frequently Asked Questions

- What is the difference between leasing and financing a car?

Leasing a car involves paying for the vehicle's depreciation over a specified period, while financing involves taking out a loan to purchase the car outright. At the end of a lease, you return the car, whereas, with financing, you own the vehicle once the loan is paid off.

- Can I negotiate the terms of a car lease?

Yes, many aspects of a car lease, such as the monthly payment, mileage limit, and money factor, can be negotiated. It's important to research and compare offers from multiple dealerships to secure the best terms.

- What happens if I exceed the mileage limit on my lease?

If you exceed the mileage limit outlined in your lease agreement, you will likely incur additional fees, typically charged per mile over the limit. To avoid these fees, choose a mileage limit that aligns with your driving habits.

- Can I buy the car at the end of the lease?

Yes, most lease agreements offer a purchase option at the end of the lease term, allowing you to buy the car at a predetermined price, often based on the residual value.

- Are lease payments tax-deductible?

Lease payments may be tax-deductible if the vehicle is used for business purposes. It's essential to consult with a tax professional to understand how leasing can impact your specific tax situation.

- What should I do if I want to end my lease early?

Ending a lease early can result in significant penalties and fees. However, some options may be available, such as transferring the lease to another party or negotiating an early termination with the dealership. Be sure to review your lease agreement and discuss your options with the leasing company.

Conclusion

Leasing cars near you can offer numerous benefits, from lower monthly payments and access to the latest models to flexibility and convenience. However, it's essential to carefully consider your needs, preferences, and budget when deciding whether leasing is the right choice for you. By understanding the leasing process, negotiating favorable terms, and avoiding common pitfalls, you can make the most of your leasing experience and enjoy the advantages of driving a new car without the long-term commitment of ownership. With the right approach and information, leasing can be a smart and fulfilling option for many drivers.

You Might Also Like

Unlocking The Secrets Of A Lush Lawn: The Ultimate Guide To Aerator LawnThe Great Gatsby PDF: A Timeless Classic In The Digital Age

10 Effective And Trustworthy Weight Loss Programs Near Me: Discover The Best Options In Your Area

Mastering The Art Of "Play It By Ear": An In-Depth Exploration

Understanding The Conversion: 2.5 Mm To Inches - Your Ultimate Guide

Article Recommendations

- Lolo Soetero

- Air Conditioning Compressor

- Wicker Outdoor Furniture

- Forest Sunlight

- Whats Akons Real Name

- Pigs Ears Mushroom

- Ghetto Bob

- 6 Cabinet Filler

- Crayola Crayon Drawing

- Planet Fitness Gyms