Life insurance provides peace of mind, ensuring that your family is financially protected in the event of your passing. The right life insurance policy can cover debts, mortgage payments, education costs, and even daily living expenses, allowing your loved ones to maintain their standard of living. Selecting the best life insurance policy requires careful consideration of your unique circumstances and financial objectives. Factors such as age, health, income, and family size all play a role in determining the most suitable policy for you. Additionally, understanding the differences between term life insurance, whole life insurance, and universal life insurance is crucial in making an informed choice. This guide will delve into these aspects, offering insights and tips to help you navigate the complex world of life insurance. As you embark on this journey to find the best life insurance, remember that it's not just about finding the cheapest option. It's about finding a policy that offers comprehensive coverage, aligns with your financial goals, and provides the security your family deserves. With the right information and resources, you can confidently choose a life insurance policy that safeguards your family's future.

| Table of Contents |

|---|

| 1. Understanding Life Insurance |

| 2. Types of Life Insurance |

| 3. Key Features of Life Insurance Policies |

| 4. Benefits of Life Insurance |

| 5. Choosing the Best Life Insurance for You |

| 6. Factors to Consider When Selecting a Policy |

| 7. How to Compare Life Insurance Policies |

| 8. Term Life Insurance Explained |

| 9. Whole Life Insurance: A Comprehensive Overview |

| 10. Universal Life Insurance: Flexibility and Benefits |

| 11. Common Myths About Life Insurance |

| 12. The Role of Health in Life Insurance |

| 13. Life Insurance Riders: Enhancing Your Coverage |

| 14. FAQs About Life Insurance |

| 15. Conclusion: Securing Your Family's Future |

Understanding Life Insurance

Life insurance is a contract between an individual and an insurance company. In exchange for premium payments, the insurer provides a lump-sum payment, known as a death benefit, to beneficiaries upon the insured's death. This financial protection can be critical in helping families cover expenses such as funeral costs, debts, and living expenses.

There are various types of life insurance, each designed to meet different needs and financial objectives. Understanding the basic principles of life insurance is the first step in choosing the best policy for you and your family.

The primary purpose of life insurance is to provide financial security for your beneficiaries. This security can help them maintain their lifestyle, pay off debts, and plan for the future even in your absence. Additionally, life insurance can be a tool for estate planning and wealth transfer, offering tax advantages and ensuring that your legacy is preserved.

Types of Life Insurance

Life insurance policies can be broadly categorized into two main types: term life insurance and permanent life insurance. Each type has distinct features, benefits, and drawbacks, making it essential to understand their differences.

Term Life Insurance

Term life insurance provides coverage for a specified period, usually ranging from 10 to 30 years. If the insured dies during the term, the beneficiaries receive the death benefit. Term life insurance is often the most affordable option, making it an attractive choice for young families or individuals with temporary financial obligations.

Permanent Life Insurance

Permanent life insurance, which includes whole life and universal life policies, offers lifelong coverage. In addition to the death benefit, these policies often build cash value over time, which can be borrowed against or withdrawn by the policyholder. Permanent life insurance is generally more expensive than term life insurance but provides additional benefits and flexibility.

Key Features of Life Insurance Policies

When evaluating life insurance policies, it's crucial to consider key features that can impact the overall value and suitability of the policy. These features include the death benefit amount, premium costs, policy duration, and any additional benefits or riders.

The death benefit is the amount paid to beneficiaries upon the insured's death. It's essential to choose a death benefit that adequately covers your family's financial needs, including mortgage payments, education costs, and living expenses.

Premium costs vary based on factors such as age, health, and policy type. While term life insurance premiums are generally lower, permanent life insurance policies offer additional benefits that may justify the higher cost.

Policy duration is another important consideration. Term life insurance provides coverage for a specific period, while permanent life insurance offers lifelong protection. Understanding your financial goals and obligations can help you determine the most appropriate policy duration.

Benefits of Life Insurance

Life insurance offers numerous benefits beyond the death benefit. It provides peace of mind, knowing that your loved ones will be financially secure in the event of your death. Additionally, life insurance can serve as a valuable estate planning tool, helping you transfer wealth to your heirs while minimizing tax liabilities.

Some life insurance policies also build cash value over time, offering a source of savings that can be accessed for various financial needs. This cash value can be borrowed against or withdrawn, providing additional financial flexibility and security.

Life insurance can also be used to cover estate taxes and other expenses, ensuring that your heirs receive the full value of your estate. By carefully planning your life insurance coverage, you can protect your family's financial future and preserve your legacy.

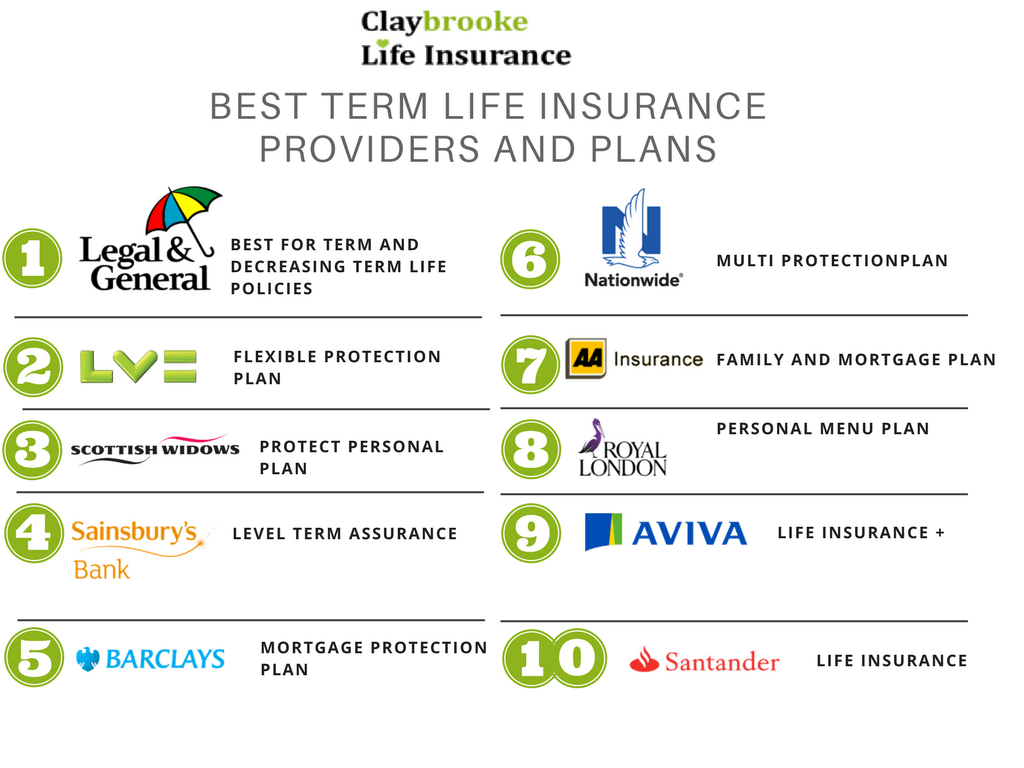

Choosing the Best Life Insurance for You

Finding the best life insurance policy requires a thorough understanding of your financial goals, family needs, and available options. Start by assessing your financial obligations, such as mortgage payments, debts, and education costs, to determine the appropriate death benefit amount.

Consider your age, health, and lifestyle when evaluating life insurance options. Younger individuals with good health may qualify for lower premiums, while those with health issues may need to explore specialized policies or riders.

Research different types of life insurance policies and compare their features, benefits, and costs. Use online resources and tools to obtain quotes and evaluate policy options from multiple insurers. Consulting with a financial advisor or insurance professional can also provide valuable insights and guidance.

Factors to Consider When Selecting a Policy

Several factors can influence your choice of life insurance policy, including your financial goals, family needs, and personal preferences. Consider the following factors when selecting a policy:

- Coverage Amount: Determine the appropriate death benefit amount based on your family's financial needs and obligations.

- Policy Duration: Choose a policy duration that aligns with your financial goals and obligations, whether it's temporary coverage or lifelong protection.

- Premium Costs: Evaluate the affordability of premiums based on your budget and potential changes in your financial situation.

- Policy Type: Consider the benefits and drawbacks of term life insurance versus permanent life insurance, based on your financial goals and preferences.

- Insurer Reputation: Research the financial stability and customer service reputation of insurance companies to ensure you're choosing a reliable provider.

How to Compare Life Insurance Policies

Comparing life insurance policies involves evaluating key features, benefits, and costs to determine the most suitable option for your needs. Use the following steps to compare policies effectively:

- Gather Information: Collect information about different policies, including coverage amounts, premium costs, policy durations, and additional benefits.

- Use Online Tools: Utilize online comparison tools and calculators to obtain quotes and compare policy options from multiple insurers.

- Evaluate Features: Assess the features and benefits of each policy, considering factors such as cash value growth, policy flexibility, and available riders.

- Consider Insurer Reputation: Research the financial stability and customer service reputation of insurance companies to ensure you're choosing a reliable provider.

- Consult with Professionals: Seek guidance from financial advisors or insurance professionals to gain insights and recommendations based on your unique situation.

Term Life Insurance Explained

Term life insurance is a type of life insurance that provides coverage for a specified period, usually ranging from 10 to 30 years. It offers a straightforward and affordable way to protect your family's financial future during the policy term.

The primary advantage of term life insurance is its affordability. Premiums are typically lower than those of permanent life insurance policies, making it an attractive option for young families or individuals with temporary financial obligations.

However, term life insurance does not build cash value, and coverage ends when the policy term expires. If you still need coverage after the term expires, you'll need to purchase a new policy, which may come with higher premiums due to age and health changes.

Whole Life Insurance: A Comprehensive Overview

Whole life insurance is a type of permanent life insurance that offers lifelong coverage and builds cash value over time. It provides a death benefit to beneficiaries and allows policyholders to accumulate savings through cash value growth.

One of the key benefits of whole life insurance is its cash value component, which grows tax-deferred and can be accessed through loans or withdrawals. This feature provides financial flexibility and can serve as a source of savings for various needs.

Whole life insurance also offers stable premiums, which remain level throughout the policyholder's lifetime. While premiums are higher than those of term life insurance, the added benefits and cash value growth can make it a valuable long-term investment.

Universal Life Insurance: Flexibility and Benefits

Universal life insurance is a type of permanent life insurance that offers flexibility in premium payments and death benefits. It combines the lifelong coverage of whole life insurance with the ability to adjust premium payments and death benefits based on your financial situation and goals.

One of the main advantages of universal life insurance is its flexibility. Policyholders can increase or decrease premium payments and adjust the death benefit amount as needed. This flexibility allows you to adapt your coverage to changing financial circumstances.

Universal life insurance also builds cash value, which grows tax-deferred and can be accessed through loans or withdrawals. This feature provides additional financial security and flexibility for policyholders.

Common Myths About Life Insurance

There are several misconceptions about life insurance that can lead to confusion and hesitation when choosing a policy. Understanding and debunking these myths can help you make informed decisions about your life insurance needs.

Myth 1: Life Insurance is Only for Breadwinners

While life insurance is crucial for primary earners, it can also provide financial protection for stay-at-home parents and others who contribute to the household. Their contributions have monetary value, and life insurance can help cover the costs of replacing their role.

Myth 2: Young, Healthy People Don't Need Life Insurance

Purchasing life insurance at a young age can lock in lower premiums and provide coverage for future financial obligations. It's never too early to plan for your family's financial security.

Myth 3: Employer-Provided Life Insurance is Sufficient

Employer-provided life insurance can be a valuable benefit, but it may not offer enough coverage to meet your family's needs. Additionally, coverage may be lost if you change jobs or retire, making a personal policy essential for long-term protection.

The Role of Health in Life Insurance

Your health plays a significant role in determining life insurance premiums and eligibility. Insurers assess your health status through medical exams and questionnaires to evaluate risk and determine premium rates.

Maintaining a healthy lifestyle can positively impact your life insurance premiums. Factors such as regular exercise, a balanced diet, and avoiding smoking can lead to lower premium costs and better coverage options.

It's important to disclose accurate health information when applying for life insurance. Failing to do so can lead to policy cancellation or denial of claims, leaving your beneficiaries without financial protection.

Life Insurance Riders: Enhancing Your Coverage

Life insurance riders are optional add-ons that can enhance your coverage and provide additional benefits. They allow you to customize your policy to better meet your financial goals and family needs.

Common Riders:

- Waiver of Premium: This rider waives premium payments if the policyholder becomes disabled and cannot work.

- Accidental Death Benefit: Provides an additional death benefit if the insured dies as a result of an accident.

- Critical Illness Rider: Offers a lump-sum payment if the insured is diagnosed with a critical illness, such as cancer or heart disease.

- Child Term Rider: Provides coverage for the policyholder's children, offering financial protection in the event of their death.

Consider your financial goals and family's needs when selecting life insurance riders. While they can increase premium costs, the added benefits and protection may be worth the investment.

FAQs About Life Insurance

1. What is the best age to buy life insurance?

It's generally best to purchase life insurance when you're young and healthy, as this can result in lower premiums and better coverage options.

2. How much life insurance coverage do I need?

The amount of coverage you need depends on your financial obligations, such as debts, mortgage payments, and living expenses. A financial advisor can help you determine the appropriate coverage amount.

3. Can I have multiple life insurance policies?

Yes, you can have multiple life insurance policies. Many individuals choose to have a combination of term and permanent policies to meet different financial goals and needs.

4. What happens if I miss a premium payment?

If you miss a premium payment, your policy may lapse, and coverage could be terminated. Some policies offer a grace period, allowing you to make a payment before coverage is lost.

5. Is life insurance taxable?

In most cases, life insurance death benefits are not subject to federal income tax. However, there may be tax implications if the policy has a cash value component or if the death benefit exceeds certain limits.

6. Can I change my life insurance policy?

Depending on your policy, you may be able to make changes, such as adjusting the death benefit or adding riders. It's important to review your policy regularly and consult with your insurer or financial advisor to make necessary adjustments.

Conclusion: Securing Your Family's Future

Choosing the best life insurance policy is a critical step in securing your family's financial future. By understanding the different types of life insurance, evaluating key features, and considering your unique needs and goals, you can make an informed decision that provides peace of mind and financial protection.

Remember, life insurance is not a one-size-fits-all solution. Take the time to research, compare policies, and consult with professionals to ensure you select the best life insurance policy for your situation. With the right coverage in place, you can rest assured that your loved ones will be financially secure, no matter what the future holds.

For additional resources and guidance on choosing the best life insurance, consider visiting reputable insurance websites or consulting with a licensed insurance agent.

You Might Also Like

The Comprehensive Guide To Hypodermic Needles: History, Usage, And ImportanceLivin La Vida Loca: A Journey Through The Crazy Life

The Marvelous Benefits And Uses Of Avocado Oil

The Remarkable Journey Of Faramir: A Tale Of Courage And Wisdom

The Versatility And Benefits Of Cedar Wood

Article Recommendations

- Lolo Soetero

- Hasselblad 553 Elx

- Tooth Lady China Concubine

- Southern Cornbread Recipe

- Empanada Dough

- 6 Cabinet Filler

- Opal Engagement Ring

- Good Earth Soil

- Nikol Johnson Wiki

- Walker Shepard