When it comes to retirement planning, understanding your options is crucial. Two popular retirement savings plans are the 401k and the 403b. Both offer tax advantages and are designed to help you save for retirement, but they have distinct differences that can impact your financial future. In this article, we will explore the key differences, benefits, and considerations of 401k vs 403b, helping you make an informed decision about which plan is right for you.

Retirement savings plans are essential for ensuring financial security in your later years. With the rising cost of living and the uncertainty of social security benefits, it’s crucial to have a robust savings strategy in place. The 401k and 403b plans are two of the most commonly used employer-sponsored retirement plans in the United States. Understanding the nuances between them can significantly affect your retirement savings journey.

This article will delve into the specifics of 401k vs 403b, including who is eligible for each plan, their contribution limits, tax implications, and withdrawal rules. By the end, you will have a comprehensive understanding of these retirement plans, allowing you to make the best choice for your financial needs.

Table of Contents

- Overview of 401k and 403b Plans

- Eligibility for 401k and 403b

- Contribution Limits

- Tax Implications of 401k and 403b

- Withdrawal Rules for 401k and 403b

- Investment Options Available

- Employer Contributions

- Which Plan is Better for You?

Overview of 401k and 403b Plans

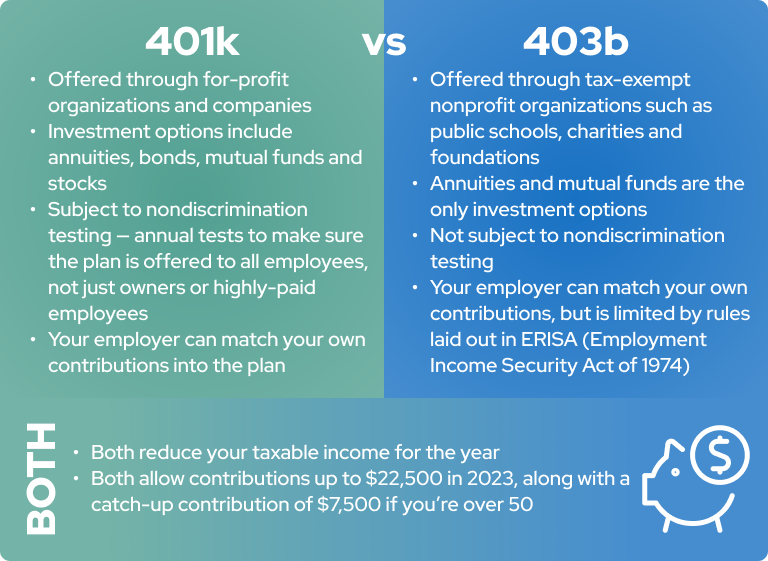

The 401k plan is a retirement savings plan offered by private-sector employers. It allows employees to save a portion of their paycheck before taxes are taken out, reducing their taxable income. On the other hand, the 403b plan is similar but is designed for employees of public schools and certain tax-exempt organizations, such as charities and non-profits.

Key Features of 401k Plans

- Available to employees of private companies.

- Employers can match contributions.

- Higher contribution limits compared to some other plans.

Key Features of 403b Plans

- Available to employees of public schools and non-profit organizations.

- May offer additional benefits like tax-free growth options.

- Lower administrative costs in some cases.

Eligibility for 401k and 403b

Eligibility for a 401k plan typically depends on the employer’s policies. Most employers require employees to be over a certain age and have completed a specific duration of employment before they can participate.

In contrast, 403b plans are specifically for employees of public schools, tax-exempt organizations, and certain ministers. This means that if you work in a non-profit or educational sector, you may qualify for a 403b.

Contribution Limits

For the year 2023, the contribution limit for both 401k and 403b plans is $22,500 for individuals under 50 years old. Those aged 50 and older can make catch-up contributions, raising their limit to $30,000.

It’s important to note that while both plans have similar contribution limits, the specifics can vary based on employer policies and additional plan features.

Tax Implications of 401k and 403b

One of the primary benefits of both 401k and 403b plans is the tax advantages they provide. Contributions to these plans are made pre-tax, which lowers your taxable income for the year. Taxes are deferred until withdrawals are made during retirement.

However, there can be differences in tax treatment based on the type of 403b plan (traditional vs. Roth). In a traditional 403b, contributions are made pre-tax, while in a Roth 403b, contributions are made after-tax, allowing for tax-free withdrawals in retirement.

Withdrawal Rules for 401k and 403b

Both 401k and 403b plans impose penalties for early withdrawals made before age 59½. Generally, a 10% penalty is applied, in addition to regular income tax. However, there are exceptions for certain circumstances, such as disability or substantial medical expenses.

Additionally, both plans require that you begin taking minimum distributions by age 72, ensuring that you utilize your retirement savings during your lifetime.

Investment Options Available

The investment options available in 401k and 403b plans can vary significantly. Typically, 401k plans offer a wider range of investment choices, including stocks, bonds, mutual funds, and sometimes even company stock.

On the other hand, 403b plans often have more limited investment options, primarily focusing on annuities and mutual funds. However, many 403b plans are improving their investment options to be more competitive with 401k plans.

Employer Contributions

Both 401k and 403b plans may offer employer contributions, which can significantly boost your retirement savings. Employers can match employee contributions up to a certain percentage, providing an added incentive for employees to save for retirement.

It’s important to review your specific plan’s employer matching policy, as this can vary widely between plans and organizations.

Which Plan is Better for You?

Deciding between a 401k and a 403b plan ultimately depends on your employment situation and financial goals. If you work for a private company, a 401k may be your only option. However, if you are employed by a public school or non-profit organization, you may have the choice between the two.

Consider factors such as employer matching contributions, investment options, and your long-term financial strategy when making your decision. Consulting with a financial advisor can also provide personalized guidance to help you choose the best retirement plan for your needs.

Conclusion

In summary, both 401k and 403b plans offer valuable benefits for retirement savings, but they cater to different types of employees. Understanding the differences in eligibility, contribution limits, tax implications, and investment options is crucial for making an informed decision. As you plan for your retirement, consider your employment situation, financial goals, and the specific features of each plan.

We encourage you to leave a comment below with your thoughts or questions, share this article with others who may benefit, or explore our other resources on retirement planning.

Final Thoughts

Retirement planning can be overwhelming, but knowing your options can empower you to take control of your financial future. Whether you choose a 401k or a 403b, the key is to start saving early and consistently. We invite you to return to our site for more insightful articles and resources on financial planning.

You Might Also Like

The Walking Dead Season 7: A Deep Dive Into The ApocalypseThe Fascinating World Of K-Dramas: An In-Depth Exploration

Pineapple Calories: A Comprehensive Guide To Nutritional Benefits

Understanding PO700 Code: Causes, Solutions, And Preventive Measures

Everything You Need To Know About Oat Milk: The Ultimate Guide

Article Recommendations

- Ella Bleu S Career Updates

- Long Handled Post Hole Diggers

- Jeremy Wariner Net Worth

- Financial Empowerment_0.xml

- Risk Territory Between Ukraine And Siberia Nyt

- Bryan Hearne

- Ruben Roman

- Madison Beer Nude Leak

- Poker Face Sunglasses

- Convert Excel To Html Table