Understanding your credit score is essential for financial health and planning. It plays a crucial role in determining your eligibility for loans, credit cards, and even rental agreements. Many individuals may wonder, "What does your credit score start at?" This article will provide a comprehensive overview of credit scores, including how they are calculated, what factors influence them, and strategies to improve your score.

Credit scores range from 300 to 850, with higher scores indicating better creditworthiness. When you start your credit journey, your score may begin at the lower end of this spectrum. However, it's crucial to understand that various factors can influence your score, making it possible to improve it over time.

This article will delve into the intricacies of credit scores, offering insight into how they affect your financial decisions and what you can do to maintain a healthy credit profile. Whether you're just starting out or looking to improve your existing credit score, this guide will provide valuable information.

Table of Contents

- What Is a Credit Score?

- How Is Your Credit Score Calculated?

- What Does Your Credit Score Start At?

- Factors Affecting Your Credit Score

- Improving Your Credit Score

- Common Misconceptions About Credit Scores

- Checking Your Credit Score

- Conclusion

What Is a Credit Score?

A credit score is a numerical representation of your creditworthiness, reflecting the likelihood that you'll repay borrowed money. Lenders use this score to assess the risk of lending you money or extending credit. Credit scores are based on data from your credit report, which includes your credit history, outstanding debts, payment history, and more.

Types of Credit Scores

There are several types of credit scores, but the two most common are:

- FICO Score: Developed by the Fair Isaac Corporation, this score is widely used by lenders.

- VantageScore: Created by the three major credit bureaus (Experian, TransUnion, and Equifax), this score also evaluates creditworthiness.

How Is Your Credit Score Calculated?

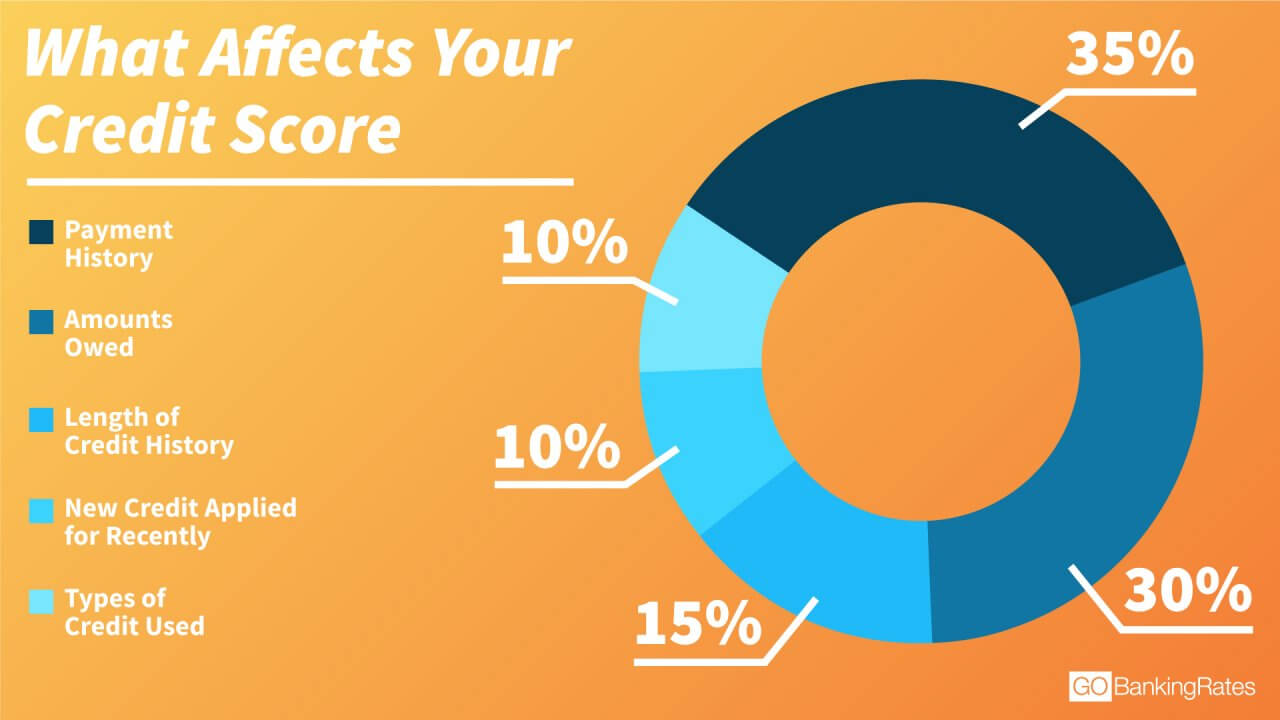

Credit scores are calculated based on several factors, each contributing a different percentage to your overall score:

- Payment History (35%): Your ability to make timely payments on loans and credit cards.

- Credit Utilization (30%): The amount of credit you're using compared to your total credit limit.

- Length of Credit History (15%): The duration of your credit accounts and how long they've been active.

- New Credit (10%): The number of recently opened credit accounts and inquiries into your credit report.

- Types of Credit (10%): The diversity of your credit accounts, including credit cards, mortgages, and installment loans.

What Does Your Credit Score Start At?

Your credit score typically starts at around 300 if you have no credit history. However, if you have a limited credit history or negative items on your report, your score may be lower. For individuals with a robust history of timely payments and responsible credit usage, scores can start higher.

It's essential to note that just because your score starts low, it doesn't mean it can't improve. Many individuals can raise their scores significantly by practicing good credit habits over time.

Starting Scores for Different Types of Borrowers

Here are some examples of what different borrowers might experience:

- New Borrowers: Often start around 300, as they have no established credit history.

- Those with Limited Credit: May start anywhere from 400 to 600, depending on their history.

- Established Borrowers: Typically start in the 600s or 700s, assuming they have a good payment history.

Factors Affecting Your Credit Score

Several factors can influence your credit score. Understanding these can help you make informed decisions about maintaining and improving your score.

1. Payment History

Your payment history is the most significant factor in your credit score. Late payments, defaults, and bankruptcies can severely damage your score.

2. Credit Utilization Ratio

This ratio measures how much credit you're using compared to your available credit. Keeping your utilization below 30% is generally recommended.

3. Credit Age

Older credit accounts can positively affect your score, as they demonstrate your experience in managing credit.

4. Recent Credit Inquiries

Each time you apply for credit, a hard inquiry is made, which can temporarily lower your score. Limit applications to avoid multiple inquiries.

Improving Your Credit Score

Improving your credit score is a gradual process, but it can be achieved through consistent effort. Here are some strategies:

- Pay Bills on Time: Make timely payments on all your debts.

- Reduce Credit Card Balances: Aim to keep your credit utilization ratio below 30%.

- Check Your Credit Report: Regularly review your credit report for errors and dispute any inaccuracies.

- Limit New Credit Applications: Avoid applying for multiple credit lines at once.

Common Misconceptions About Credit Scores

There are many myths surrounding credit scores that can lead to confusion. Here are a few common misconceptions:

- Checking Your Own Score Hurts It: Checking your own credit score is a soft inquiry and does not affect your score.

- Closing Old Accounts Improves Your Score: Closing old accounts can negatively impact your credit age and utilization ratio.

- All Debt Is Bad: Not all debt is detrimental; responsible use of credit can positively influence your score.

Checking Your Credit Score

Monitoring your credit score is essential for staying informed about your financial health. You can check your score through various platforms, including:

- Credit reporting agencies (Experian, TransUnion, Equifax)

- Financial institutions that offer free credit score monitoring

- Dedicated credit score websites

Conclusion

Your credit score is a fundamental aspect of your financial life, starting typically at around 300 for new borrowers. Understanding how your score is calculated and what factors influence it is essential for maintaining a healthy financial profile. By practicing good credit habits and staying informed, you can improve your credit score over time.

If you found this article helpful, please leave a comment or share it with others who may benefit. Explore our other articles for more insights into financial health and credit management!

Additional Resources

For further reading and resources, consider visiting the following websites:

Thank you for reading, and we hope to see you back for more financial insights!

You Might Also Like

Do Dogs Have Feelings? Understanding The Emotional Lives Of Our Canine CompanionsUnderstanding Debt Relief Programs: Your Comprehensive Guide

How To Find The Circumference Of A Circle: A Comprehensive Guide

96 Acura Integra: A Comprehensive Guide To The Iconic Sports Car

How To Effectively Increase Your Credit Score: A Comprehensive Guide

Article Recommendations

- Growth Hacking_0.xml

- Chevy S10 Steering Wheel

- Bang On Casino

- Kamila Valieva

- Collision Repair Before And After

- Tumblr Fashion Male

- Chandie Yawn Nelson

- Mia Hamm Soccer Player

- Mario Lopez

- Poker Face Sunglasses