When planning for retirement, choosing the right type of 401(k) can significantly impact your financial future. The decision between a Roth and Traditional 401(k) is one of the most crucial choices you’ll face as you prepare for your golden years. Understanding the key differences between these two retirement savings options will help you make an informed decision that aligns with your financial goals.

In this comprehensive guide, we will explore the features, benefits, and drawbacks of both Roth and Traditional 401(k) plans. By the end of this article, you'll have a clear understanding of which retirement plan suits your needs best. We’ll break down the tax implications, contribution limits, withdrawal rules, and more, providing you with the necessary information to navigate your retirement planning effectively.

Whether you're just starting your career or are nearing retirement, the choice between a Roth and Traditional 401(k) can have long-lasting effects on your savings. Let’s dive into the details to help you determine the best option for your financial future.

Table of Contents

- Understanding 401(k) Plans

- What is a Roth 401(k)?

- What is a Traditional 401(k)?

- Key Differences Between Roth and Traditional 401(k)

- Tax Implications of Each Plan

- Withdrawal Rules and Penalties

- Who Should Choose Which Option?

- Making the Right Choice for Your Future

Understanding 401(k) Plans

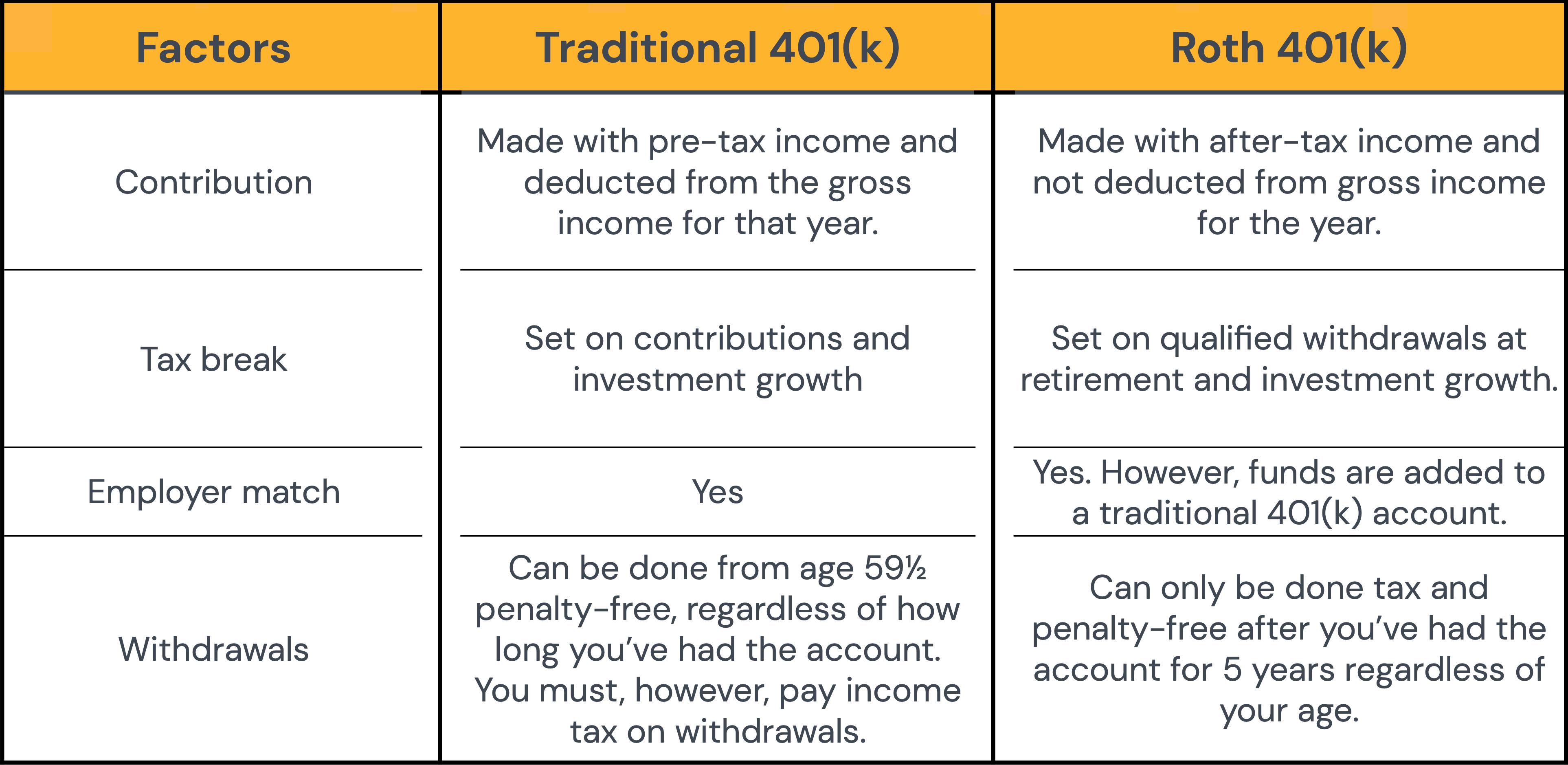

A 401(k) plan is a workplace retirement savings plan that allows employees to save a portion of their paycheck before taxes are taken out. It is named after the section of the Internal Revenue Code that governs it. Employers often match a portion of employee contributions, providing additional incentives to save for retirement.

There are two primary types of 401(k) plans: Traditional and Roth. Each plan has unique features that cater to different financial situations and retirement goals. Understanding these differences is essential for making an informed choice.

What is a Roth 401(k)?

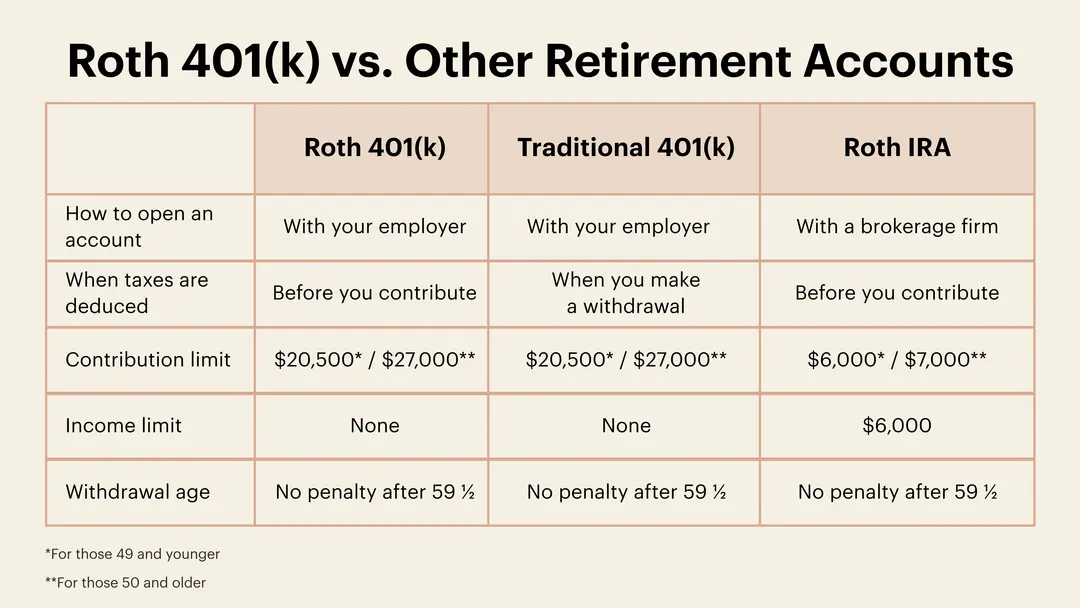

A Roth 401(k) is a retirement savings plan that allows employees to contribute after-tax dollars to their accounts. This means that contributions are made from your salary after taxes have been deducted. The primary advantage of a Roth 401(k) is that withdrawals, including earnings, are tax-free in retirement, provided certain conditions are met.

Benefits of a Roth 401(k)

- Tax-free growth: Earnings grow tax-free, potentially resulting in substantial savings over time.

- No required minimum distributions (RMDs): Unlike Traditional 401(k) plans, Roth 401(k)s do not require withdrawals during the account holder's lifetime.

- Flexibility in retirement: Tax-free withdrawals provide flexibility in managing your tax bracket during retirement.

What is a Traditional 401(k)?

A Traditional 401(k) allows employees to contribute pre-tax dollars to their retirement savings. This means contributions are made before income taxes are deducted, reducing the employee's taxable income for the year the contributions are made. However, withdrawals during retirement are subject to income tax.

Benefits of a Traditional 401(k)

- Tax-deferred growth: Investments grow tax-deferred until withdrawal, potentially resulting in a larger account balance at retirement.

- Lower taxable income: Contributions reduce your taxable income, which may result in immediate tax savings.

- Employer matching: Many employers offer matching contributions, providing additional funds to your retirement savings.

Key Differences Between Roth and Traditional 401(k)

Understanding the key differences between Roth and Traditional 401(k) plans can help you make an informed decision about which option is best for you. Here are the primary distinctions:

1. Tax Treatment

- Roth 401(k): Contributions are made with after-tax dollars, and withdrawals (including earnings) are tax-free in retirement.

- Traditional 401(k): Contributions are made with pre-tax dollars, and withdrawals are taxed as ordinary income in retirement.

2. Withdrawal Rules

- Roth 401(k): Withdrawals can be made tax-free if the account has been open for at least five years and the account holder is at least 59½ years old.

- Traditional 401(k): Withdrawals are subject to income tax and potential penalties if taken before age 59½, unless certain conditions are met.

3. Required Minimum Distributions (RMDs)

- Roth 401(k): No RMDs are required during the account holder's lifetime.

- Traditional 401(k): RMDs must begin at age 72, whether or not the account holder needs the funds.

Tax Implications of Each Plan

When considering a Roth vs. Traditional 401(k), it’s essential to understand the tax implications of each option. The choice you make can impact your overall tax liability during both your working years and retirement.

Roth 401(k) Tax Implications

Contributions to a Roth 401(k) do not provide a tax break in the year they are made, as they are funded with after-tax income. However, the benefit comes during retirement when you can withdraw funds tax-free. This is particularly advantageous if you expect to be in a higher tax bracket in retirement.

Traditional 401(k) Tax Implications

Contributions to a Traditional 401(k) reduce your taxable income for the year they are made, which can yield immediate tax savings. However, withdrawals in retirement will be taxed as ordinary income, which could result in a higher tax bill if your income is substantial.

Withdrawal Rules and Penalties

Understanding the withdrawal rules and penalties associated with each type of 401(k) is crucial for effective retirement planning.

Roth 401(k) Withdrawal Rules

- Contributions can be withdrawn at any time without penalty.

- Tax-free qualified distributions can be made after age 59½ and after the account has been open for five years.

- Early withdrawals of earnings may be subject to taxes and penalties.

Traditional 401(k) Withdrawal Rules

- Withdrawals can begin at age 59½ without penalty.

- Withdrawals before age 59½ may incur a 10% early withdrawal penalty, in addition to income tax.

- RMDs must begin by age 72, regardless of whether the account holder needs the funds.

Who Should Choose Which Option?

Determining whether a Roth or Traditional 401(k) is right for you depends on your current financial situation and future income expectations.

When to Choose a Roth 401(k)

- If you expect to be in a higher tax bracket in retirement.

- If you want tax-free withdrawals and no RMDs during your lifetime.

- If you have a long time horizon for your investments to grow tax-free.

When to Choose a Traditional 401(k)

- If you want to reduce your taxable income in the present.

- If you expect to be in a lower tax bracket in retirement.

- If you anticipate needing to withdraw funds before age 59½.

Making the Right Choice for Your Future

Choosing between a Roth and Traditional 401(k) requires careful consideration of your financial goals and circumstances. It may also be beneficial to consult with a financial advisor to evaluate your options based on your unique situation. Here are a few strategies to consider:

- Diversify your retirement accounts: Consider contributing to both types of accounts to benefit from tax diversification.

- Review your tax situation: Analyze your current and projected future tax brackets to make an informed choice

You Might Also Like

Baby Generator: The Ultimate Guide To Creating Your Dream FamilyUltimate Guide To MCU Movies: Everything You Need To Know

What Is Instagram? A Comprehensive Guide To The Social Media Giant

Where Do I Watch Kdrama: The Ultimate Guide To Streaming Korean Dramas

What Is Sticky Rice? A Comprehensive Guide To This Unique Grain

Article Recommendations

- Lava Stone Bracelet Essential Oil

- How To Make Raphael In Infinite Craft

- Legal Seafood Recipes Crab Cakes

- Streaming Device Whose Name Means Six

- Balanced Lifestyle_0.xml

- Water Softener Overflowing Brine Tank

- Risk Territory Between Ukraine And Siberia Nyt

- Ella Bleu S Career Updates

- Corinne Foxx

- Healthy Habits_0.xml