In the world of retirement planning, understanding the differences between various savings options is crucial for long-term financial success. One of the most common comparisons that arise is between the 401a and 401k retirement plans. Both options offer unique benefits and features tailored to different employment situations and financial goals. By diving into the specifics of each plan, you can make an informed decision that aligns with your retirement objectives.

The 401a plan is often provided by government agencies and non-profit organizations, while the 401k plan is more frequently associated with private-sector employers. As we explore the distinctions between these two retirement plans, it is essential to evaluate their structure, contribution limits, tax implications, and withdrawal options. By understanding these key factors, you can effectively navigate your retirement savings strategy.

In this article, we will delve deep into the 401a vs 401k debate, highlighting the essential features, advantages, and disadvantages of each plan. We will also examine how to choose the right option for your unique circumstances and financial goals. So, let's get started on this journey to better understand your retirement planning options!

Table of Contents

- What is a 401a Plan?

- What is a 401k Plan?

- Key Differences Between 401a and 401k Plans

- Contribution Limits for 401a and 401k

- Tax Implications of 401a and 401k Plans

- Withdrawal Options and Penalties

- Which Plan is Right for You?

- Conclusion

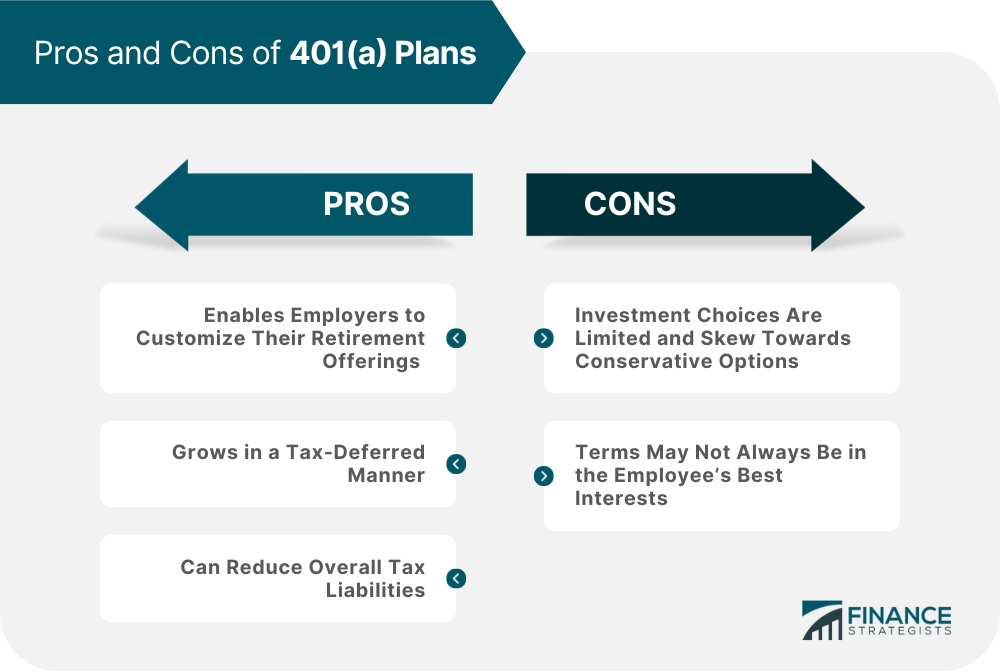

What is a 401a Plan?

A 401a plan is a type of retirement savings plan that is typically offered by government employers or certain non-profit organizations. It allows employees to contribute a portion of their salary to a tax-deferred account, which grows over time and can be withdrawn during retirement. Here are some key features of a 401a plan:

- Employer Contributions: Employers often make contributions to the plan on behalf of employees, which can be a fixed percentage of the employee's salary.

- Vesting Schedule: Employees may need to meet specific requirements to fully own employer contributions.

- Investment Options: 401a plans may offer various investment options, including mutual funds and annuities.

What is a 401k Plan?

A 401k plan is a popular employer-sponsored retirement savings plan that allows employees to save a portion of their income for retirement on a tax-deferred basis. Here are some key features of a 401k plan:

- Employee Contributions: Employees can choose to contribute a percentage of their salary, often matched by employers up to a certain limit.

- Flexible Investment Options: Employees typically have a wide range of investment choices, allowing them to tailor their portfolio to their risk tolerance and retirement goals.

- Loan Options: Some 401k plans allow participants to borrow against their balance for emergencies or significant expenses.

Key Differences Between 401a and 401k Plans

Understanding the differences between 401a and 401k plans is essential for making informed retirement decisions. Here are some critical distinctions:

- Eligibility: 401a plans are generally available to employees of government and non-profit organizations, whereas 401k plans are offered by private-sector employers.

- Contribution Structure: 401a plans often involve employer contributions, while 401k plans rely on employee contributions, potentially matched by employers.

- Vesting Requirements: 401a plans may have strict vesting schedules for employer contributions, while 401k plans often allow immediate access to employee contributions.

Contribution Limits for 401a and 401k

The contribution limits for both 401a and 401k plans are determined by the IRS and can change annually. As of the latest data:

- The contribution limit for a 401k plan is $19,500 for individuals under 50 years old and $26,000 for those aged 50 and older.

- The contribution limit for a 401a plan can vary based on employer policies but is generally subject to the same overall contribution limits as a 401k.

Tax Implications of 401a and 401k Plans

Both 401a and 401k plans offer tax advantages that can significantly impact your retirement savings. Here are the key tax implications:

- Tax-Deferred Growth: Contributions to both plans grow tax-deferred until withdrawal, allowing for potentially greater accumulation over time.

- Taxable Withdrawals: Withdrawals from either plan are subject to income tax, which can affect your tax bracket in retirement.

- Early Withdrawal Penalties: Early withdrawals (before age 59½) may incur a 10% penalty in addition to income tax.

Withdrawal Options and Penalties

Understanding withdrawal options and penalties is crucial for effective retirement planning. Here’s a breakdown:

- 401a Plans: Withdrawals may be limited to certain qualifying events, such as retirement, disability, or termination of employment.

- 401k Plans: Participants typically have more flexibility in accessing funds, including hardship withdrawals and loans.

- Penalties: Both plans impose penalties for early withdrawals, emphasizing the importance of long-term planning.

Which Plan is Right for You?

Choosing between a 401a and a 401k plan depends on various factors, including your employment status, financial goals, and retirement strategy. Here are some considerations:

- If you work for a government agency or non-profit organization, a 401a plan may be your primary option.

- If you are employed in the private sector, a 401k plan may offer greater flexibility and contribution options.

- Consider your long-term financial goals, investment preferences, and retirement timeline when making your decision.

Conclusion

In summary, both 401a and 401k plans serve as valuable retirement savings vehicles, each with its own set of features and benefits. By understanding the differences between these plans, you can make informed decisions that align with your financial goals and retirement strategy. Whether you choose a 401a or a 401k, the key is to start saving early and make the most of the tax advantages these plans offer.

We encourage you to leave a comment below sharing your thoughts or experiences with 401a and 401k plans. Additionally, feel free to share this article with others who may benefit from this information or explore other articles on our site for more insights into retirement planning.

Thank you for reading, and we look forward to seeing you back on our site for more valuable financial insights!

You Might Also Like

Mango Juul Pod: The Ultimate Guide To Flavor And ExperienceBest Wallets: A Comprehensive Guide To Choosing The Right One

Understanding The Types Of Checks: A Comprehensive Guide

Fagioli Pronunciation: A Comprehensive Guide To Mastering This Italian Term

Understanding RACI Chart: A Comprehensive Guide For Effective Project Management

Article Recommendations

- Piper Parabo

- Future Opportunities_0.xml

- Lax Plane Spotting Locations

- Arianna Lima 2024

- Risk Territory Between Ukraine And Siberia Nyt

- Bang On Casino

- Jeremy Wariner Net Worth

- Kylie Jenner Before Surgery

- Poker Face Sunglasses

- Brand Building_0.xml